How not to Overpay, Invest like a Peter Lynch, CG Issue (IT Raid) Live case study and How to deal with it, Important Learning from 4 Hour long Marathon Meet

How not to Overpay, Invest like a Peter Lynch, CG Issue (IT Raid) Live case study and How to deal with it, Important Learning from 4 Hour long Marathon Meet

Premium Issue - 24

Hi, Welcome to the 24th Special Premium Edition

Brief Overview of What We will cover in this Issue

Detailed Key Takeaways from the book I am reading Currently

5 Decent Articles to read and Key Takeaways from them.

Key Takeaways From Long Interview with one of the best fund manager

Boring Investing (Best One)

Learn how to invest like Peter Lynch

What they don’t tell you about those Compounding Stories - Harsh Truths (Video Clip)

CG Issue(IT Raid) Live Case Study (What to do in this situation)(Video Clip)

The margin of safety/ How not to overpay (The Best Video Clip)

➢ Now you can buy single issues as well if you just want to read specific Newsletter issues only or wanted to read before subscribing to full-year plan, Click Here to buy today’s 24th Special Edition

I Publish 4-5 quality Posts per month (2 Free, 2 Paid) so be assured that I take care in adding value to my free subscribers as well as paid ones. Do not unsubscribe in anticipation of the only paid newsletter :) will send a Free post Next Saturday

If you are a free subscriber but want to read the full issue, Do Subscribe to Paid Plan (If there is any error in payment then contact me at Twitter DM)

(Please choose to read a direct post from Our Blog to avoid missing some of the last section of content)The Simple Path to Wealth (Part-2)

The Big Ugly Event

There, in 1929, is the Big Ugly Event. The Mother of all Stock Market Crashes and the beginning of the Great Depression. Over a two-year period, stocks plunged from 391 to 41, losing 90% of their value along the way. Should you have been unlucky enough to have invested at the peak, your portfolio wouldn’t have fully recovered until the mid-1950s, 26 years later. Yikes. That’s enough to try the toughest investor.

If you had been buying stocks on margin (that is, with money borrowed from your broker) as was all too common at the time, you would have been completely wiped out. Many speculators were. Fortunes were lost overnight. Never buy stocks on margin.

So what to do? Does the possibility of another Big Ugly Event blow a big enough hole in this idea of “toughen up and ride out the storms” to make it useless? The answer to that has everything to do with your tolerance for risk and your desire to build wealth. There are ways to mitigate the risk and we’ll talk about them later.

For now, let’s step back and consider a few key points regarding The Big Ugly:

1. It would have taken an investor of exceptionally bad luck to have borne the full weight of the crash. You would have had to buy your entire portfolio precisely at the 1929 peak.

Suppose instead you had invested in 1926-27. Looking at our chart this is about halfway up on the climb to the peak. Many, many people were entering the market in these years. Certainly, they were destined to lose all their gains, and yet 10 years later, had they held on, they’d be back in positive territory. Although another rough stretch was coming.

Suppose you’d bought at the earlier peak in 1920. You would have taken an immediate hit and recovered five years later. From the collapse in ’29 you’d be back even by 1936. Seven years.

The point is that any given start would have yielded a different outcome and one not as severe as the widely quoted 90% loss, peak to bottom.

2. Suppose you were just out of school and beginning your career in 1929. Assuming you were in the fortunate 75% that kept their jobs, you would have had decades of opportunities to buy stocks at bargain prices. Ironically, a crash at the beginning of your investing life is a gift. In fact, any pullback in stock prices is a gift while you are in the process of accumulating your wealth. It allows you to buy more shares for your dollars, on sale if you will.

3. Suppose in 1929 you were retired with a million dollars. By 1932 your portfolio is down 90%, to $100,000. A terrible hit for sure. But remember, the Depression was a deflationary event. That means the prices of goods and services fell dramatically, along with those of stocks. And that means your $100,000, while no longer a million, now had far more buying power than that same amount did pre-crash. Plus, it was poised to grow rather sharply from this low.

4. The Big Ugly Event has happened only once in the last 115 years. Longer actually, but that’s how far back our DJIA data goes. We haven’t had another in 86 years. Some even argue that with the controls put in place since 1929 it is unlikely we ever will again. While we can’t be sure of that, we do know these are extremely rare events.

Little inflation can be a very healthy thing for an economy. It allows for prices and wages to expand. It keeps the economic wheels greased and running smoothly. It is the antidote to looming deflationary depressions

In a deflationary environment, delayed buying decisions are rewarded. If you were considering a new house in 2009-13 you would have noticed that prices were dropping, along with mortgage interest rates. Recognizing you could get both for less later, you waited. If enough potential buyers joined you, demand would drop pulling prices and rates down further. Delay is rewarded and action is punished.

But during periods of inflation, anything you want to buy will cost more tomorrow than today. You have the incentive to buy that house (or car or appliance or a loaf of bread) today and beat the price increase. Delay is punished with higher prices later and action now is rewarded.

None of this is to say that Big Ugly Events are not very scary and destructive things. But they are rare and in the context of our overriding approach (spend less than you earn—invest the surplus—avoid debt), they are survivable.

Keeping it simple: Considerations and tools Simple is good. Simple is easier. Simple is more profitable.

That’s a key mantra of this book and what I’m going to share with you in these next couple of chapters is the soul of simplicity. With it, you’ll learn all you need to know to produce better investment results than at least 82% of the professionals and active amateurs out there.

How can this be? Isn’t investing complicated? Don’t I need professionals to guide me? No and no.

Since the days of Babylon people have been coming up with investments, mostly to sell to other people. There is a strong financial incentive to make these investments complex and mysterious.

But the simple truth is this: the more complex an investment is, the less likely it is to be profitable.

Index funds outperform actively managed funds in large part simply because actively managed funds require expensive active managers. Not only are they prone to making investing mistakes, but their fees are also a continual performance drag on the portfolio.

But they are very profitable for the companies that run them, and as such are heavily promoted.

Safety is a bit of an illusion

There is no risk-free investment. Once you begin to accumulate wealth, the risk is a fact of life. You can’t avoid it, you only get to choose what kind. Don’t let anyone tell you differently. If you bury your cash in the backyard (or in an FDIC-insured bank account at today’s near-zero interest rates) and dig it up 20 years from now, you’ll still have the same amount of money. But even modest inflation levels will have drastically reduced its spending power. If you invest in stocks, you’ll likely outpace inflation and build wealth but you’ll have to endure a volatile ride.

Remember that nothing money can buy is more important than your fiscal freedom. In this modern world of ours, no tool is more important.

Index funds are really just for lazy people, right?

No. Index investing is for people who want the best possible results.

Indeed, over periods of 15 to 30 years, the index will outperform 82% to 99% of actively managed funds. This means that just buying a total stock market index fund like VTSAX guarantees you’ll be in the top performance tier. Year after year. Not bad for accepting “average.” I can live (and prosper) with that kind of average.

But investing is a long-term game. You’ll have no better luck picking and switching winning managers than winning stocks over the decades.

People underestimate the drag of costs to investing.

As Bogle says, performance comes and goes but expenses are always there, year after year. After year. Compounded over time the amount lost is breathtaking.

People want quick results, excitement, and bragging rights. They want the thrill of victory and to boast about their stock that tripled or their fund that beat the S&P 500. Letting an index work its magic over the years isn’t very exciting. It is only very profitable. (Why Index fund is boring)

As for me, I seek my excitement elsewhere and let indexing do the heavy lifting of my wealth-building.

Finally— and perhaps most influential— there is a huge business dedicated to selling advice and brokering trades to people who can be persuaded to believe they can outperform. Money managers, mutual fund companies, financial advisers, stock analysts, newsletters, blogs, and brokers all want their hands in your pocket. Billions are at stake and the drumbeat marketing the idea of outperformance is relentless. In short: we are brainwashed.

Let me take a moment to be absolutely clear. I don’t favor indexing just because it is easier, although it is. Or because it is simpler, although it is that too. I favor it because it is more effective and more powerful in building wealth than the alternatives.

I’d happily put in more effort for more return. More effort for less return? Not so much.

Inflation/Deflation

Bonds are in our portfolio to provide a deflation hedge. Deflation is one of the two big macro risks to your money. Inflation is the other and we hedge against that with our stocks. You’ll recall from earlier that deflation occurs when the price of goods spirals downward and inflation occurs when they soar. Yin and yang.

In times of inflation, prices rise and so money owed to you loses value. When you get paid back your cash buys less stuff. Then it is better to own assets, like stocks, that rise in value with inflation.

Portfolio ideas to build and keep your wealth

Life is balance and choice. Add more of this, lose a little of that. When it comes to investing, that balance and choice is informed by your temperament and goals.

Complex and expensive investments are not only unnecessary, but they also underperform. Fiddling with your investments almost always leads to worse results. Making a few sound choices and letting them run is the essence of success and the soul of The Simple Path to Wealth.

Selecting your asset allocation

Risk Factors: Temperament. This is your personal ability to handle risk. Only you can decide and if ever there was a time to be brutally honest with yourself, this is it.

Age: As you age you steadily have less time for the compounding growth of your investments to work and to recover from market plunges. Both these considerations will influence your risk profile and you might well want to consider adding bonds a bit earlier if that’s the case.

Maybe you don’t want to deal with this level of volatility. Maybe a bit more peace of mind is required. As you get older you might want to smooth the ride a bit, even at the cost of lower overall returns. You want to sleep at night.

Rebalance: I’ve yet to see any credible research indicating a particular time of year works best. Personally, we rebalance once a year on my wife’s birthday. Random and easy to remember.

Does frequent reallocation improve performance?

Mr. Bogle points to research Vanguard has done comparing stock and bond portfolios that were annually rebalanced and those not rebalanced at all. The results show the rebalanced portfolios outperformed but by a margin so slight it can be attributed to noise as much as the strategy. His conclusion:

“Rebalancing is a personal choice, not a choice that statistics can validate. There’s certainly nothing the matter with doing it (although I don’t do it myself), but also no reason to slavishly worry about small changes in the equity ratio.”

Why I don’t like investment advisors

It’s your money and no one will care for it better than you. But many will try hard to make it theirs. Don’t let it happen.

Now, I’m sure there are many honest, diligent, hard -working advisors who selflessly put their client's needs ahead of their own. Actually, I am not at all sure about that. But just in case, I put it out there in fairness to the few.

By design, structurally an advisor’s interests and that of their clients are in opposition. There is far more money to be made selling complex fee-laden investments than there is in simple low-cost efficient ones. To do what’s best for the client requires the advisor to do what is not best for himself. It takes a rare and saintly person to behave this way.

Advisors are drawn not to the best investments, but to those that pay the highest commissions and management fees. Indeed, often they are compelled by their firms to sell these types of investments. Such investments are, by definition, expensive to buy and own. And investments that are expensive to buy and own are, by definition, poor investments.

Further, since these funds are most often actively managed, they carry a high expense ratio and are mostly doomed to underperform the simple low-cost index funds we can so easily buy on our own.

Hedge funds and private investments all make their salespeople wealthy, along with the operators. Investors? Maybe. Sometimes. Nah, not so much.

You not only give up the 2% each year, but you also give up all the money that money would have earned compounding for you over the 20-year period.

The great irony of successful investing is that simple is cheaper and more profitable. Complicated investments only benefit the people and companies that sell them.

“Wisdom comes from experience. Experience is often a result of lack of wisdom.”—Terry Pratchett

Jack Bogle and the bashing of index funds

While no one ever has, if someone were to ask me what single thing has most impeded the growth of my personal wealth the answer would be my stubborn rejection of the concept of indexing for an embarrassingly long number of years.

Before Mr. Bogle, the financial industry was set up almost exclusively to enrich those selling financial products at the expense of their customers. It mostly still is.

Then Mr. Bogle came along and exposed industry stock-picking and advice as worthless at best, harmful at worst and always an expensive drag on the growth of your wealth. Not surprisingly, Wall Street howled in protest and vilified him incessantly.

The basic concept behind Vanguard is that an investment firm’s interests should be aligned with those of its shareholders. This was a stunning idea at the time and to this day it is the only firm that is, and as such is the only firm I recommend.

The basic concept behind indexing is that, since the odds of selecting stocks that outperform is so very small, better results will be achieved by buying every stock in a given index. This was soundly ridiculed at the time and in some quarters it still is.

In the Berkshire Hathaway 2013 annual shareholder letter, Buffett writes: “My advice … could not be more simple: Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. (I suggest Vanguard’s.) I believe the trust’s long-term results from this policy will be superior to those attained by most investors – whether pension funds, institutions or individuals – who employ high-fee managers

There is still about 4,600 equity (stock) mutual funds being offered as of this writing. To put this in perspective, there are only about 3,700 publicly traded U.S. companies in them to invest in. Yes, you read that correctly. As we saw in Part II, there are more stock mutual funds out there than there are stocks for them to buy.

Wall Street is endlessly creating new products and schemes to sell you, even as they systematically and quietly close those that have failed

Research House/Investment Firms

They knew each of these industries, and the companies in them, inside and out. They knew the top executives. They knew the middle managers and the front-line people. They knew the customers. They knew the suppliers. They knew the receptionists. They spoke to them all weekly. Sometimes daily.

They still didn’t get critical information before anyone else (that’s insider trading and foolproof, but illegal).

You know what Warren Buffett recommends for individual investors: Low-cost, broad-based index funds. Graham, were he still alive, would too

How to be a stock market guru and get on CNBC

The key thing his program and its parade of guests taught me is that, at any given time, some expert is predicting any possible future that could conceivably happen. Since all bases are covered, someone is bound to be right. When they are, their good luck will be interpreted as wisdom and insight. If their prediction happened to be dramatic enough, it could also lead to fame and fortune.

keep in mind that once your guru status is established, you’ll be expected to be able to repeat it. For months—maybe years—everything you say will be noted. Each misstep will be gleefully documented until you slip from view humiliated and discredited. But also rich if you’ve played your moment in the sun well

You, too, can be conned

Rule #1: Everybody can be conned. Certainly, stupid people are marks. But so are the exceptionally bright. The moment you start to think that it can’t happen to you, You’ve become a most attractive target. The easiest victims are those that think they are too smart and too knowledgeable to be taken. This means you, bucko.

Rule #2: You are likely to be conned in an area of your expertise. The reason is simple: Targeting and ego. When con men pick a scam they look for people to whom it will naturally appeal.

Smart people know the areas they don’t know and tend to be far more cautious there. Many of Bernie Madoff’s victims were financial professionals.

Rule #3: 99% of what they say will be true. The best, most effective lies are surrounded by truth. Buried in it

Rule #4: If it looks too good to be true, it is. There is no free lunch. Not ever.

“Money frees you from doing things you dislike. Since I dislike doing nearly everything, money is handy.”—Groucho Marx

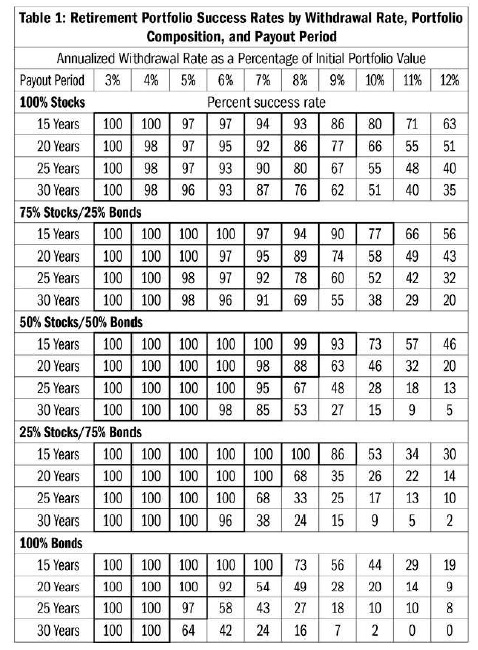

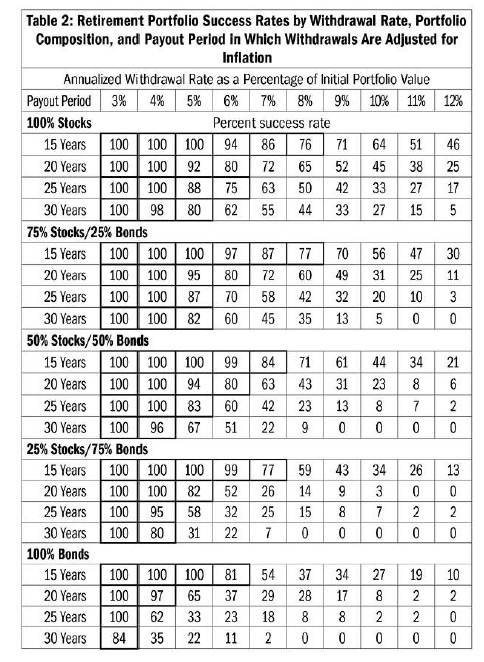

Withdrawal rates: How much can I spend anyway?

Back in 1998, three professors from Trinity University sat down and ran a bunch of numbers. Basically, they asked what would happen at various withdrawal percentage rates to various portfolios, each with a different mix of stocks and bonds, over 30-year periods depending on what year the withdrawals were started. They ran their scenarios both adjusting withdrawal levels for inflation and not adjusting the withdrawal. Whew. Then they updated it in 2009.

The 4% withdrawal rate, 50/50 stock/bond portfolio, adjusted for inflation. Turns out, 96% of the time, at the end of 30 years such a portfolio remained intact. there was just a 4% chance of this strategy failing and leaving you destitute in your old age. (1965 and 1966 were the last and only two years where 4% failed)

If you are curious, here’s an overview of the Trinity Study you can read for yourself: Click Here

Inflation Adjusted 👇

So if you look at Table 1 and at the 50/50 mix with a 4% withdrawal rate, you see you have a 100% chance of your portfolio surviving 30 years.

Table 2 tells you that if you take those same parameters but give yourself inflation raises, your portfolio’s chance of survival drops to 96%.

How do I pull my 4%?

→ First, we think about the non-investment income we still have coming in. Even once you are “retired,” if you are actively engaged in the life you might well also be actively engaged in things that create some cash flow. We are no longer in savings mode, but this earned money is what gets spent first. And to the extent it does, it allows us to draw less from our investments and allows them in turn still more time to grow.

→ We keep a simple spreadsheet and log in our expenses by category as they occur. This allows us to see where the money is going and to think about where we might cut should the market plunge and the need arise.

My path for my kid: The first 10 years

Avoid debt. Nothing is worth paying interest to own.

Avoid fiscally irresponsible people and certainly don’t marry one.

Spend the next decade or so working your ass off building your career and your professional reputation.

Don’t get trapped by an expanding lifestyle or unwind it if you already are.

Save and invest at least 50% of your income. Put this in VTSAX or one of the other options we’ve discussed in this book.

Save more than 50% and you’ll get there sooner. Save less and it will take a bit longer.

If you get lucky with the market you’ll get there sooner. If not, it will take a bit longer.

During this accumulation phase, celebrate market drops. While you are in the wealth accumulation phase, these are gifts. Each dollar you invest will buy you more shares.

But never fall prey to thinking you (or anyone else) can anticipate or time these drops.

Once 4% of your assets can cover your expenses, consider yourself financially independent. Put another way, financial independence = 25x your annual expenses. That is, if you are living on $ 20,000 you have reached financial independence with $ 500,000 invested.

It’s never too late. It took me decades to figure this stuff out. Like mine, your road has likely already had more bumps than those who follow this path from the start will endure. But those bumps are in the past. It is your future that matters and that starts, for all of us, right now.

Some final thoughts on risk

F-You Money. With it, the world’s possibilities are endless and you are faced with the delicious decision as to what to do with your freedom. The only limits are your imagination and your fears.

Stocks are considered very risky, and they are certainly volatile in the short term. But go out 5-10 years and the odds strongly favor handsome returns. Go out 20 years and you are virtually guaranteed to be made wealthier by owning them. At least if the last 120 tumultuous years are any guide

Stocks have far more volatility than cash and in return provide far more wealth-building potential. Cash has little volatility, but you pay for that in the slow erosion of its spending power.

If you have the money you have risk. You don’t get to choose not to have risk, you only get to choose what kind.

We all must play the odds and make our decisions based on the alternatives. But in doing so we must also realize that fear and risk are often overblown, and understand that letting our fear control us carries its own set of risks. Getting past my own fears has allowed me to avoid panic and ride out financial disasters like the one that occurred in 2008. It has given me my own F-You Money.

Having come this far, you now have a solid understanding of how investing really works and how to realistically build your wealth. You also now understand that the road can be rocky and that plunges in the market are normal. Armed with this knowledge, such events begin to lose their power to create fear in you, allowing you to avoid panic and stay focused on your goal of building wealth and achieving financial freedom.

The Path is before you. You need only take the first step and begin. Enjoy your journey!

Excerpts and Learning from Articles/Blogs

1) A Few Good Stories

Focusing on what’s never going to change is more important than trying to anticipate how something might change.

life is about probabilities, not certainties.

Everything good in life is just the gap between expectations and reality.

Most decisions aren’t made on a spreadsheet, where you just add up the numbers and a rational answer pops out. There’s a human element that’s hard to quantify, hard to explain, and can seem totally detached from the original goal, yet carries more influence than anything else.

The best story – not the most prepared, or the most thought out, or the most analytical – wins.

2) Interview With Mid-Cap Mogul Kenneth Andrade

→ Avoiding Big Investing Mistakes

Invest in what you know

One way of avoiding mistakes is to understand what you do, that way you can identify and correct it when and if it does go wrong. If you don’t know the investment, you would never know if things are going wrong in the first place.

→ Why Most investors don’t succeed in Stock Market

I guess most serious investors do succeed in markets. The longer you stay invested, the better the results. Investing needs to be passive and rather than focus on prices investors should concentrate on the underlying. A lot of investors give up in the short term.

→ Market Volatility

you need to use volatility to your advantage. Markets overshoot in both directions, and if you take advantage of this it could be extremely profitable. But one needs the discipline to take advantage of these extremities.

→ The key criteria for fund selection?

Investing in any portfolio should be a long-term commitment. Likewise, the long-term is also associated with durability. So if one needs to buy an MF scheme for the long term, the portfolio also needs to be in sync. Portfolio churn is never good for the long-term investor.

→ MF vs DIY

The error that most investors commit is the discipline of diversification. If this were managed well the outcomes would not be very different from diversified mutual funds

→ Investing Style

No one style fits all. But by sticking to what you understand best will give you more upsides than downs. Don’t diversify your style.

As investors, we all consistently focused on return. On the contrary, we should be risk managers. A bull market gives you a return because all stocks participate; a manager has very little role in that. It is the downside that counts.

You have to have a framework that works in a market offering you negative returns and measure your successes by buying companies that survive an economic slide.

→ Scalability of Business/ Red Flag to watch out

A company's profit is limited by the size of its industry. Hence my fetish for scale sets in. Off course, once this scale is established, the execution has to be profitable market share growth.

In my framework any company that loses market share raises a red flag, the cost of building back market share gains is ridiculously expensive. It is an easy parameter for most investors to track. (This framework may not strictly apply to commoditized businesses, but it works in most cases).

→ Capital Cycle/Business Cycles

Demand creates profitability, which creates market caps which in turn creates the need for fresh capacity. So in this framework, companies, which were growing 15%-20% per annum, set up capacities to grow between 30%-50% using near-term historical numbers to justify the capital investment. This creates excessive capacities. This is why the same sectors get very capital-intensive and never return to historic levels of capital efficiency and then valuations.

If the above is true, we would need to let go of the past and look at industries where supply constraints or competitive intensity is low. Chances are they hold on to their profits and efficient capital allocation. One way of tracking this is leverage. Banks usually are arbitragers of high capital-efficient businesses and low-interest rates. They usually fund excessive creation of capacity based again of near-term historical numbers, which they extrapolate into the future. So look for what these institutions fund, it may be the beginning of the next economic bubble; and excessive lending may end up being the end of one.

→ How can one analyze companies to find efficient use of capital? and how does one create a list of such companies

In one of the questions above I alluded to two components of the capital efficiency ratio – the numerator and the denominator (ROE = PAT/ Shareholder Capital; ROCE = PBIT/ Capital Employed). The numerator is profitability, which largely is the function of the economy; I don’t believe I can predict a complex subject of growth.

The denominator however is the function of the management and efficient capital allocation. A lower denominator is all I look for and you don’t need a model to predict that. This is already in the public domain. Just look for the latter. If you buy a portfolio of 20 companies that meet this criterion, the probability of going wrong is well zero!

→ Books Recommendation

→ Sources for Deep Dive in Business Analysis

And nothing beats company annual reports if you want to deep dive into an analysis of a company.

3) Boring is Beautiful in Investing

The more exciting your portfolio, the worse your performance is in this bear market.

“All portfolio problems stem from investor’s inability to stick with a boring old asset allocation.”

Successful investing should be boring. It should be long-term in nature. It requires patience and discipline and the ability to ignore the madness of the crowds.

You’re never going to get rich overnight investing in index funds or housing.

But index funds don’t have an ego.

They’re never going to return your money to spend more time with their family.

Index funds won’t see their performance impacted by going through a nasty divorce.

They won’t commit fraud against you or gate your withdrawals or transfer your money from one company to the next to cover losses made from idiotic mistakes.

A high savings rate combined with a bunch of boring, low-cost, tax-efficient investments is the margin of safety I needed before ever even considering a riskier investment profile.

One of my biggest takeaways after nearly 20 years of working in the markets is survival is an underrated quality for success.

Exciting stuff doesn’t always work. Nothing does.

You need the boring stuff as a ballast in your portfolio because the boring stuff always comes back in style.

When the boring stuff doesn’t work it usually means underperformance.

When the exciting stuff doesn’t work, you can lose all of your money.

4) Ensemble Capital Investor Letter – Third Quarter 2022

Recessions occur every seven to 10 years, the odds of a recession in any randomly selected year is about 10%-15%. This is true even when there are no obvious signs that a significant economic slowdown is around the corner

Investors without a sense of history may intuitively assume that all recessions are like the Great Financial Crisis of 2008-09, during which the stock market was cut in half and the economy collapsed. But that recession was, in fact, the worst recession since the Great Depression and not at all representative of an average recession. During mild recessions, the stock market has typically declined by 15% to 30%, a magnitude of decline already witnessed this year. During severe recessions, stock market declines have been on the order of 30% to 50%.

Over the last 40 years, there have been only four recessions or about one per decade.

This framework for thinking about recession risks and equity market returns is identical to what we discussed in the fourth quarter of 2018 when recession worries gripped the market and the S&P 500 had declined by 20% over just 10 weeks. When those recession fears proved to be misplaced and the economy continued to power forward, the stock market ripped higher by 47% from the late 2018 lows through early 2020

Because investors cannot count on their ability to accurately predict recessions, we believe the best course of action for equity investors is to own high-quality companies that are protected by strong competitive advantages, have very capable management teams, and are prudent in their risk-taking such that there is never any question that they can make it through recessions when they inevitably arrive.

Investing in the 1970 Bear Market

5) 23-page Playbook to learn how to invest like Peter Lynch.

Small Video Clips

➢ Prashant Jain Interview by Udayan Mukherjee (BT)

Prashant Jain on New Age Business (03:18 to 04:33)

View on PSU & Defence Sector (05:06 to 08:06)

Errors of omission/Mistakes and thought on that (15:02 to 16:48)

➢ PPFAS Mutual Fund Unitholders' Meet 2022 (Our Own Berkshire Meet)

Watched the Entire 4-Hour Mega Session! I Never feel bored watching PPFAS Meet.

Also, They did my work already by separating the full video into 60 Parts so Here I will share important & favorite clips Here

Optimize returns in long term, Don't maximize returns in the short term (Good Parameter to check Fund/Fund Manager) (11:50 To 16:04)

Golden Investing Rules (18:59 to 22:51)

Hero MotoCorp CG Issue(IT Raid) Case Study (What to do in this situation)

Good discussion on why they have not invested in Tesla & Other EV Manufacturing Companies

Understanding of Price sales ratio and WB's Market Cap to GDP Ratio

(Refer to Jim O'Shaughnessy’s thoughts on the Same Topic, Shared Here)

Reasons behind the basket approach investing in Pharma Sector

Not sharing Stock Specific Clips Here, You can watch them Here if you want.

➢ The Art Of Investing w/ François Rochon (William Green) Worth Watching Entire Conversion

The margin of safety/ How not to overpay (21:13 to 24:54) The Best Part

His market-beating investment journey

How to succeed by investing in great companies at reasonable valuations

How to survive & thrive by taking a middle-of-the-road approach to diversification.

How he was influenced by studying & meeting investment icon Peter Lynch, Low Simpson

If you are interested then here is his shareholder letters completion done by Leandro