सार (Lessons and Key Takeaways): 30+ Years of Investing

सार (Lessons and Key Takeaways): 30+ Years of Investing

Free Issue No. #033

Welcome to the 180 new members who have joined us since the last Free Issue. Join the 4470+ others who are receiving awesome content related to investing and Important Key learning from Great Investing books

Great Books Offers Running Now, Do visit this thread to know about great deals (Up-to 60-70%)

Market veteran Prashant Jain in his 30-year journey’s Saar, meaning summary in Hindi, touched upon unsettled issues such as debate over active and passive funds and discussions over PSU stocks, and also wrote about his success and mistakes, in addition to his key learnings that helped him become one of the most successful fund managers in India.

Here is the full, unedited text of सार (read as 'saar', which means essence), a note written by Jain over a month after he resigned from his position:

The journey from Managing 10 Crore to 100000 Crore

HDFC Balanced Advantage Fund (BAF) over the years. On turning open ended in 1999, the Fund shrank to a mere Rs 9.9 crore (1 crore: 10 million), probably because the NAV was above par. From this to approximately Rs 46,000 crore in July 2022 when I handed over the reins of this Fund has been a journey beyond my imagination – made possible among other things by this period coinciding with the coming of age of mutual funds in India

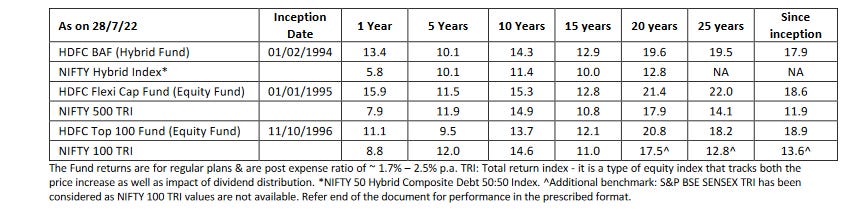

This Fund has delivered a CAGR of 17.91% in this 28 years 7 months. The Fund was also at the top of peer group in its category as on 28th July 2022 across time periods from 1 year to 25 years

This reminds one of what Einstein observed – Compound interest is the 8th wonder of the world, those who understand it, they earn it, those who don’t, they pay it.

I was also managing HDFC Flexi Cap Fund since 2003 (for approximately 19 years) and HDFC Top 100 Fund since 1999 (for approximately 23 years). The table below gives a summary of the performance of these funds as on 28 th July, 2022 in five year buckets and since inception

The Pareto Principle

While pursuing PGDM at IIM Bangalore in 1989-1991, I was introduced to this principle. It states that typically 20% of the effort gives 80% of the results and vice versa. My experience with investing is a good illustration of this.

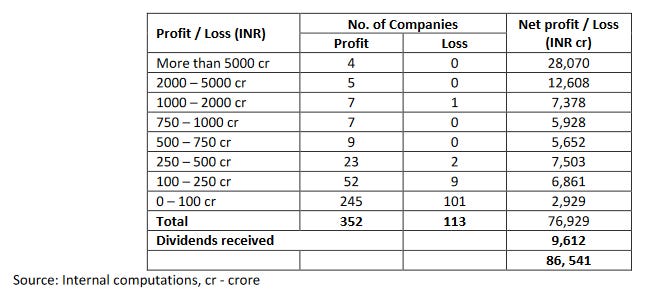

The table below gives a summary of the scorecard (distribution of gains / losses) between October 2003-July 2022 across the 3 funds that I managed

Investments were made in a total of 465 stocks. One in four resulted in a loss. Of the total net gains of approximately 87,000 crores (including dividends), 55 stocks accounted for a gain of more than 74,000 crores (including estimated dividends) i.e. 85% of total. If only one had the wisdom of avoiding 90% of the investments and instead invested more in the 55 stocks !

Fortunately, I not only persisted with the portfolio positioning but doubled down in some cases as with the adverse price movement, risk reward had become more compelling. Over time as normalcy returned, the performance recovered strongly and quickly. The pain of few years was gone in a few quarters

Markets can be driven by emotion and herd behaviour for extended periods and thus keep on throwing opportunities once in a while. The best opportunities are to found either in most difficult market conditions or in most polarized markets. Investing is, thus, more about emotional quotient than about IQ

Sizing is very important: Any portfolio will have its share of big winners, winners, losers and big losers. In my case roughly 1/4 were losers, 1/100 were big losers, 1/20 were big winners and the rest were winners. However, it is interesting to note that gains on one large winner were more than the total losses of all loss making investments. This highlights the importance of sizing – of assessment of the risk-reward associated with individual investments and sizing accordingly.

Markets are reasonably efficient over long periods. The duration of mispricing or

inefficiency can vary from several quarters to several years. It is important in this period to stay the course and to remain solvent

Fortunately, the longer the mispricing, typically the higher is the catchup. Markets thus reward in most cases for the entire of period of pain. The only catch here is that the intrinsic value of the business per share should not erode in this phase.

Equities are a generous asset class. The tailwind of a growing economy and growing companies overshadows mistakes of timing and security selection in diversified portfolios in most cases over long periods. The key is patience to stay invested for long periods.

Significant divergence of portfolios from benchmarks and consequently a higher tracking error (that many equate to risk, though there are strong arguments to the contrary) will be needed in many cases to overcome the hurdle of costs and to generate alpha over long periods in my judgment.

Herd behaviour and the majority opinion is more often wrong than right.

The assets under my management crossed Rs 100,000 crores few days before I tendered my resignation – I take this as a divine nudge to me to make way for others.

The last word:

I don’t have words to describe the incredible journey of last 30 years. Looking back at the sequence of events, I honestly feel that I was incredibly lucky to be at the right place at the right time not once but on several occasions. Whenever I was about to take a wrong turn, some invisible hand nudged me in the right direction. The only credit I can take is that of doing my best every single day. I wouldn’t mind doing it all over again

- Prashant Jain

Sources:

1. सार - Last Note by Mr. Prashant Jain

2. What Prashant Jain said on his mistakes

3. Hits, misses and a dash of nostalgia in Prashant Jain's farewell note

These 2 Books Covered Prashant Jain’s Journey and His experience and Key Learning

1. How Fund Managers are Making You Rich: Discover Ways to Tame the Bear and Ride the Bull

2. India’s Money Monarchs: Conversations with leading investors

Terry Smith’s Owners Manual – 13 Filters For Purchasing A Great Investment

That’s it from my end for this week.

Thanks for reading.

See you again next week!

Dhaval.

If you enjoyed this, please share it with your friend.

Great read!

Nice article