Simple Ways to Stop Doing Dumb Things with Money and Learnings from other Investor's Mistakes

Simple Ways to Stop Doing Dumb Things with Money and Learnings from other Investor's Mistakes

Premium Issue - 15

Hi, Welcome to the 15th Special Edition

Brief Overview of What We will cover in this Issue

Detailed Key Takeaways from the book I am reading Currently

4-5 Decent Articles to read and Key Takeaways from them.

Very Underrated Investing Video (Interview of FM from Renowned MF House with Timestamps of Important Key Learning

Wisdom from Charlie Munger on various topics like inflation, Fossil Fuel, Investing

Crash of Growth Stocks Proved why valuations matter a lot (Video Clip)

I Publish only 4-5 quality Posts per month (2 Free, 2 Paid) so be assured that I take care in adding value to my free subscribers as well as paid ones. Do not unsubscribe in anticipation of the only paid newsletter :) will send a Free post Next Saturday

Prime Day Decent Books Deal

If you want to read the full issue, Do Subscribe to Paid Plan (If there is any error then contact me at Twitter DM)

(Note: Gmail will truncate emails that are more than 102KB so please prefer to read a direct post from Our Blog to avoid missing some of the last section of content)

The Behavior Gap: Simple Ways to Stop Doing Dumb Things with Money (Part-1 Continue)

If an investment performs well, we like to think, “I picked a winner.” And hey, it’s nice to take credit when things go well.

But when one of our investments tanks, it’s someone else’s fault. We blame the guy who sold it to us, the rogue investment bankers who wrecked the economy, out-of-control government spending, lies in the media, bad weather in Brazil… just about any scapegoat will do.

And we can’t blame the investment for our decisions. At some point, we must accept responsibility. Otherwise, we’ll keep making the same mistake.

insanity is when you keep doing the same thing (in this case, blaming your investments for your losses) and expect a different result (in this case, good returns). Let’s stop acting crazy.

For starters, there’s that natural tendency of ours to avoid pain and seek pleasure. Beyond that, we’re downright terrible at predicting the future.

Boom-and-bust cycles are largely a function of our collective expectations.

Expectations drive our behavior— but they are almost always wrong.

Typically, expectations are based on our recent—often our very recent—experiences. One day, your neighbor’s house sells for a big profit. Then your brother’s house sells for an even bigger profit. Things have changed. After a while, you adjust your expectations. You now think (assume) that values will continue to rise. And you start to behave differently based on those expectations.

History is so important. It has been said that the three most important words in the English language are “remember, remember, remember.”

You’d think such events would be easy to recall. But we sometimes push such memories aside— especially when things are going well. Truth is, we like the new trend. When home prices were rising, we were really happy about it. Why worry about the past when the present is so pleasant?

Historian and philosopher George Santayana said (more or less), that those who don’t remember the past just get hammered again and again.

A Little Experience Can Be a Dangerous Thing When we ignore history, we end up basing our actions on our own limited experience. That can be very dangerous.

Many investors now approaching retirement came of age back at the beginning of the greatest bull market in history— which began almost thirty years ago. They figured investing was easy. So they took on more and more risk. Then the clouds rolled in.

Mountains are dangerous. That doesn’t mean you don’t go climbing (although maybe you don’t). But it does mean that if you want to stay alive you’d better respect those dangers.

The same is true of stocks. They’re dangerous. When we pretend otherwise, we get into trouble.

Our natural reaction is to sell after bad news (when the market is already down) and buy when news is good (after the market is already up), thus indulging our fear and our greed. It’s an impossible strategy.

Overconfidence is a very serious problem. If you don’t think it affects you, that’s probably because you’re overconfident.

In fact, the people who are most overconfident are the ones least likely to recognize it.

We can recognize that we’re not as smart as we think we are. In fact, the smartest investors are the ones who acknowledge that they’re not smart enough to forecast events or pick the best stock or avoid every scam or…

The next time you’re about to make an investment decision because you’re sure you’re right, take the time to have what I call the OC (Overconfidence Conversation). It’s been a truly powerful tool to help people in their decisions.

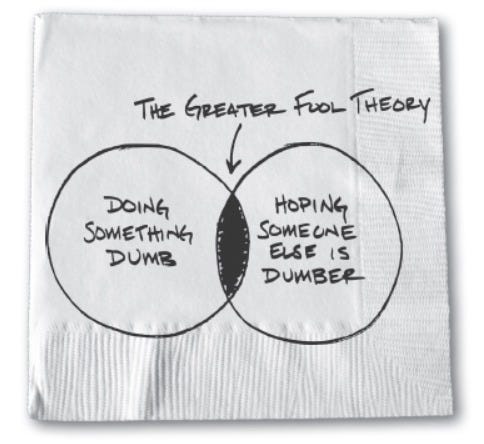

Many investors in technology stocks knew the shares they bought were hugely overvalued— but they bought them anyway. Why? Because they figured they would find some idiot (the Greater Fool of stock market lore), and sell the stock to him at an even more ridiculous price. But what happens when we run out of Greater Fools?

Before you invest your hard-earned money, ask yourself: Are you buying a particular investment because you think it’s a good investment? Or are you relying on a Greater Fool to come along? If so, doesn’t that make you— no offense— a bit foolish yourself?

We’ve been doing this for a long time. We do it because we make investing decisions based on how we feel rather than what we know.

Falling stocks scare us; rising stocks attract us.

If you find yourself routinely buying or selling at the wrong time, it’s time to do something different. One alternative— admittedly a pretty drastic one— is to swear off the stock market forever.

You’ll just be following Will Rogers’s advice: focus on the return of your money instead of the return on your money.

Face the fact that cash is not a solution to a crisis.

Normally, people go to cash to alleviate their stress: they just can’t handle the pain anymore. But when you sell you have a new problem: when to get back in. The most common “solution” to that problem is to buy back in when things have “cleared up.” Of course, when things have “cleared up,” the market will be higher. So what we’re talking about is engaging in a plan to sell low (now) and buy high (later) on purpose.

Focus on your own behavior, not the market’s behavior.

Notice the implication that the market is “doing” something right now. In reality, we only know what the market has already done. It may be peaking or bottoming out and ready to reverse course.

We don’t know what comes next for the financial markets. In the end, our own behavior is all that we can control— and ultimately, our behavior can make a huge difference in our financial success and our personal happiness.

THE PERFECT INVESTMENT

No single investment is right for everyone. The best investments for you depend on personal factors—your goals, your personality, your existing holdings, your credit card balance… The list is endless.

I often meet people who believe they’re properly diversified because they own fifteen or twenty mutual funds. But different funds can have very similar investment strategies. And when the value of one fund falls, the shares of funds with similar strategies will fall as well.

Remember, you’re not a collector. You’re an investor. You want investments that work together to close the gap between you and your financial goals. You also need to make sure that what you own doesn’t expose you to more risk than you can handle.

The researchers recommend something a bit stronger: “Do not expect the fund’s quoted past performance to continue in the future. Our studies show that mutual funds that have outperformed their peers in the past generally do not outperform them in the future. Strong past performance is often a matter of chance.

Trying to figure out which fund will lead the pack during the next quarter or next year or next decade is a fool’s game. Focus instead on finding a low-cost investment that you can stick with over the long haul.

Looking for the next hot stock is bad enough. Investing in today’s hot stock is even worse.

When making good investment decisions, it helps to be emotionally prepared for a painful result. But you need to keep making good decisions anyway. In the end, that’s a better strategy than making bad decisions.

Decisions should be based on principles, not on our feelings about what’s going to happen.

It’s always a bad idea to have too much of your net worth wrapped up in a single investment, let alone a single stock.

IGNORE ADVICE, MAKE FUN OF FORECASTS

We all like giving advice. It makes us feel needed, useful, and important. But let’s face it: most of the advice we give (and get) is useless or worse.

People tend to give you advice that’s based on their own fears, their own experience, their own expertise, and their own motivations. Their advice typically has little to do with the reality of your life. Even our friends and family, who presumably know us fairly well, usually get it wrong.

Most of the advice we come across in the media is even worse. It typically has little or nothing to do with the reality of our lives. How could it, when the person giving the advice doesn’t even know

Rules of thumb are dangerous, especially when they come from people who don’t know you.

As for that famous financial planning personality, he may be a genius. He may have helped a lot of people. But remember: He doesn’t know you. He is not your financial planner.

The financial press, personal finance bloggers, and best-selling authors are all sources of information. They may have good ideas, which you may find useful. But they can’t tell you how the information and the ideas apply to your situation.

Personal Finance is more personal than it is finance.” It’s true. Planning for your financial future is personal. It has to be. A good plan will be unique to your situation, and what is right for your situation may be a disaster for your neighbor.

So ponder how the advice you encounter applies to you before you make important decisions about your money.

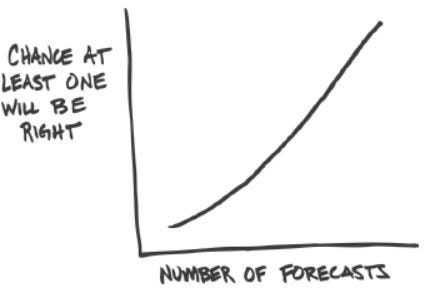

Even a broken clock is right twice a day. So don’t take it too seriously when someone calls a market turn correctly. Most likely, it’s luck.

Denrell and Fang concluded that economists who correctly call the most unexpected events have worse long-term records than the rest of the pack. In fact, they noted that the analyst with the largest number and the highest proportion of accurate extreme forecasts had by far the worst overall forecasting record. Makes sense when you think about it. The guys who tend to make bold forecasts tend to be wrong— because they’re constantly out on a limb. Once in a while, they’re right, and then they look like geniuses. More often, they’re just out there in left field.

We get interested in predictions because we’re human. A number of factors conspire to make us easy marks for forecasters.

For one thing, our survival instinct means that we’re constantly trying to predict what danger may be lurking in the bushes. And since we’re social animals, we love being in the know.

We love being the ones to break the news on Facebook or Twitter.

On a primal level, we want to be the (highly valued) person who warns others of danger or offers them useful information.

Maybe we can learn a few general principles from Buffet. But most of us are not going to invest like Buffett, no matter how many books we read.

I hate to break it to you: You’re not Warren Buffett. You’re not even the next WarrenBuffett. Fortunately, you don’t have to be. You can be you.

FINANCIAL LIFE PLANNING

Happiness is more about expectations and desire than it is about income.

Money plays no role in happiness. Money can certainly relieve stress, and reduced stress can certainly lead to increased happiness. So there is some correlation, but it seems pretty fuzzy to me. I wonder if linking happiness to money might be part of this continuing obsession we seem to have with measuring, comparing, and competing. As far as I can tell there is no unit of “happy.” We have no standard quantitative way to measure it. But if we link happiness to money, that is something we all understand. It gives me a way to compare my level of happiness to yours.

The same doesn’t apply to that amazing trip you took with your family. The trip may last for only a few days, but the memories you create will bring you greater happiness throughout your life than the gadget you picked up at the store last week.

Maybe happiness comes easiest when we are so busy working, taking care of kids, shoveling snow, or cleaning the house that we forget to look for it.

TOO MUCH INFORMATION

when everyone is buying something, it’s probably expensive (and therefore risky to own). And when everyone is selling something, it’s probably cheap (and therefore potentially appealing).

When we do what everyone else is doing, we can take comfort in knowing that even if we’re wrong, we’ll be wrong with a bunch of other people.

This kind of behavior—following the crowd— can have disastrous results. It led investors to load up on tech stocks in the late 1990s, bonds in 2002, and real estate in 2006. And yet we keep doing it, and the behavior gap grows.

That Magazine Is Not Your Financial Advisor

You shouldn’t make investment decisions based on what you see at the newsstand.

Watching stock market shows on CNBC, and poring over financial forecasts take a lot of time. Worse, it makes people anxious— and anxious people often screw up. Anxious people tend to buy high (they’re worried because they’re missing the big gains) and sell low (they worry the losses will keep piling up).

Anxious people seek comfort in familiarity.

It is becoming harder and harder to separate the signal from the noise. Most of us want to know what’s going on in the world. We feel like it’s our duty to be informed citizens, to watch the world markets, to stay on top of politics, and to keep up with the wide world of sports. If we don’t, we might miss something or be left out of the conversation.

Unfortunately, the sheer quantity of information makes it virtually impossible to sift through all the noise (most of it is just that) and find the stuff that actually matters.

At a certain point, we become addicted to information that we hope will make us feel better. Trouble is, it often makes us feel worse— and eventually, we act on our fears.

The solution: change our habits. We need to spend less time watching and worrying about our money— less time giving in to our anxiety, and our need to control things. If we can do that, we’ll soon realize that it’s not important to know what happened on Wall Street this week. What matters is what we did or didn’t

Try it. The next time you turn on the news, think long and hard about how you want to act instead of just reacting. In fact, think about whether you really need to watch the news that day.

When the Dow hit 12000 in early 2011 (before it dropped again), there was a great deal of media discussion about what this benchmark meant for investors. But who really cares? It’s just a number. We all might as well have skipped

After a day or two without access to news, I came down with a really strange rash. There were two doctors on the trip. They claimed that it might have something to do with media detoxification. I’m still not sure if they were kidding or not.

Something crazy is always happening on the other side of the world, but what does that have to do with you? You can’t do anything about it. You— and the world— are better off if you focus on what you can do.

Nothing bad will happen if you miss the endless commentary on the latest Fed announcement, I promise. If investment success is truly about behaving correctly over the long term and choosing investments within the context of your plan, what happens in the market day to day should have no impact on your decision-making.

Excerpts and Learning from Articles/Blogs

Charlie Munger on Number Calculations

Munger had this to say about the tendency to focus too much on the calculations

"Organized common (or uncommon) sense -- very basic knowledge -- is an enormously powerful tool. There are huge dangers with computers. People calculate too much and think too little."

Munger: "You really have to understand the company and its competitive positions. ...That's not disclosed by the math.

Buffett: "I don't know how I would manage money if I had to do it just on the numbers."

Munger, interrupting, "You'd do it badly."

Big mistakes are likely to get made by the investor who looks only at, -- or, at least, mostly at -- the numbers while ignoring the more qualitative things like, for example, industry dynamics. An industry with a particular set of characteristics -- even if for a very long time -- may change.

The investment process is necessarily subjective and imprecise. Both qualitative and quantitative factors have to be fully integrated with the former often being more significant than the latter.

The margin of safety can, up to a point, account for the some of unknowns and uncertainties. Yet even something as important as always buying with a sufficient margin of safety has its limits. Sometimes the worst-case scenario, even if not very probable, is simply intolerable.

So, in the context of an investment portfolio, it becomes necessary to forgo a big possible gain to keep something really bad from happening.

A fund manager’s (DSP) Investing mistakes and Learning and His Investing Philosophy - A good write-up

Most new-age stocks are ponzi schemes, warns Saurabh Mukherjea

The most dangerous form of investing people do is try to use macroeconomics, inflation, recession, and central bank actions for stock selection and investment strategy.

Even professionals do that. It is lethal. It is futile and it is basically a dangerous way to invest.

The simplest way and most powerful way to invest is to look for quality and clean franchises and stay invested. Do not get lost in this macro noise. Our belief is that macroeconomics should not be used as a way to construct investment strategy.

If the share price has gone up, you should not be happy. If the share price has gone down, you should not be depressed. The share price of a company contains zero informational value

One of the most basic and the most counterintuitive things to learn about investing is that the share price of a company follows a random walk. It means that the share price of a company is basically like a drunk man swaying his way through the street at night. If he turns left, it does not mean his house on the left. If he turns right, it does not mean he is looking for a taxi on the right. He is just a drunk man swaying his way through the night and that is the share price chart of a company.A lot of people attribute some astrological significance to it. We obviously believe that is not quite the right thing to do. Our focus is therefore not on the share price but on accounts, capital allocation and the franchise.

Key Notes Recent Charlie Munger’s Interview

Small Video Clips

How the Crash of overvalued growth stocks proves again that valuation matters the most (Guy Spier) (01:01:26 to 01:06:14)

Guy Spier on Indian Companies (IEX, CERA, Crisil, Care Rating) and insights on positing Sizing (01:22:41 to 1:35:05)

Samir Arora on Commodity Investing (36:03 to 39:43)

A very interesting view on Auto Sector (EV) by Kenneth Andrade

How Brands controlling our mind (off-topic)

Importance of knowing stock and sector Specific History and valuation trends (9:01 to 11:30) - Masterclass Video, Would recommend everyone to watch full video (Very Underrated Investing Interview, Hardly anyone shared on SM)

How to generate stock ideas (12:53 To 16:27)

Why you must read Annual Report and What to read in Annual Report (29:40 to 36:50)

How to understand real fundamentals of business beyond AR and Con-call (37:25 to 42:48)

3 Reasons when PPFAS MF Sells the Portfolio stocks (Raunak Onkar) (57:26 to 59:19)

How to avoid biases in investing field (1:02:22 to 1:07:46)