The Education of a Value Investor

Premium Issue - 7

Welcome to the 80 new members who have joined us since last Saturday. Join the 2460+ others who are receiving awesome stories related to investing and life from brilliant books

Brief Overview of What We will cover in this Issue

Detailed Key Takeaways from the book I am reading Currently

Key Takeaways from Investing Articles and Blogs

10 investing lessons from Bill Ruane

Warren Buffett's Investment Strategy (+3 Articles)

Small Important Investing Video Clips

The Intelligent Investor Approach to market

All about New-Age IPO, Complete different view of IPO (How Companies Market Narratives) (+ Many Clips)

This is freemium issue if you want to receive premium issue do upgrade to a paid plan (10% Off if you subscribe from this link)

The Education of a Value Investor

This book is about my journey from that dark place toward the Nirvana where I now live. - Guy Spier

Guy Spier’s Transformation as an Investor

A series of transformations and self-realizations led him on a path from BenjaminGraham’s The Intelligent Investor to Ruane Cunniff to PoorCharlie’s Almanack to Robert Cialdini, then to meeting Mohnish Pabrai and lunch with Warren Buffett. That $ 650,100 meal had a life-changing impact on him, as you will see. Warren Buffett has had an extraordinary impact on how Guy Spier invests and on the way, he lives his life.

Try to learn from your mistakes— better yet, learn from the mistakes of others!- Warren Buffett

If you learn only some of the lessons here, you cannot help but become rich— and perhaps wildly rich.

investing is about much more than money. So as your wealth grows, I hope you will also come to realize that money is largely irrelevant. And what you will want to do with the bulk of your wealth is give it back to society.

Instant Gratification

In addition to my arrogance and hubris, I also had my fair share of Wall Street greed. I was convinced that I was on the quick path to Nirvana.

The harsh reality was that companies with technologies or innovations that really worked and were certain to succeed were extremely rare— even among the crowd that got its funding from more prominent investment banks like Goldman Sachs and Morgan Stanley. Guy Spier was supposed to dress up the least sketchy of these deals in such a way that the downsides were heavily de-emphasized or ignored while the sizzle— the blue-sky upside— was highlighted.

Sometimes because of external environment you also fail so don't give up

During the tech bubble of the late 1990s, lousy companies were talked up and sold to an unsuspecting public. For example, analysts like Henry Blodget at Merrill Lynch were wildly bullish about Internet stocks, dressing up pigs with lipstick. Years later, the same thing happened at credit-rating agencies where analysts issued blindly positive ratings for the CMOs and CDOs that would ultimately lead to the housing crisis.

Investing Mistakes are good (कुछ दाग अच्छे होते है)

It’s a great question that can also be asked about business and investing. Warren Buffett made one of his bigger mistakes when, in his thirties, he invested in the loss-making Berkshire Hathaway textile mills. This could have been his undoing, but he later transformed Berkshire Hathaway into the towering monument of his life. He did so in part by learning to invest in better businesses instead of betting on the cigar-butt stocks (like Berkshire) that Ben Graham had taught him to buy.

An essential component of our education is to learn from our mistakes— and if we don’t make mistakes, sometimes we may not learn at all.

Guy Spier on The Intelligent Investor Book

I picked up Ben Graham’s seminal book, The Intelligent Investor, featuring a preface by Buffett. I could not put it down. Graham spoke eloquently of owning a stock not as a piece of paper to trade, but as a share in a real business. He also talked of treating“ Mr. Market” like a manic depressive and taking advantage of his shifting moods. As the market veers between fear and greed, investors can profit richly by focusing in a clearheaded way on the intrinsic value of a company and exploiting the discrepancy between the price and the value. Sometimes you know in your bones that something is true. To me, this value-investing philosophy made so much sense that it was self-evident.

Investing is simple but not easy

So many of us went into finance with tremendous confidence in our intelligence and abilities, only to discover that the system we became part of was capable of causing more harm than good.

Mohnish Pabrai: Biggest Influencer in Guy Spier’s Life

The person who has influenced me most as an investor is Mohnish Pabrai, an Indian immigrant to the United States who has racked up far better returns than I have. He studied at Clemson University in South Carolina, not at Oxford or Harvard.

The entire pursuit of value investing requires you to see where the crowd is wrong so that you can profit from their misperceptions. Value investors have to be able to go their own way.

To become a good investor, You would need to come to an acceptance of yourself as an outsider. The real goal, perhaps, is not acceptance by others, but acceptance of oneself.

The efficient Market Hypothesis is a myth

The most important example of this is the efficient-markets hypothesis, which is a powerful and theoretically useful assumption about how the world works. This hypothesis holds that financial prices reflect all of the information available to participants in the market. That has profound implications for investors. If it were true, there would be no bargains in the stock market since any price anomalies would be instantly arbitraged away. In the real world, this is simply not true. But it took Guy Spier a decade to realize it.

Be A Learning Machine

what makes Warren himself so successful is that he’s never stopped seeking to improve himself and that he continues to be a learning machine. As Munger has said,“ Warren is better in his 70s and 80s, in many ways, than he was when he was younger. If you keep learning all the time, you have a wonderful advantage.”

Guy Spier and Tonny Robbins (Authenticity)

Robbins won me over in part by being transparent about his motives. At one point, he told us, “Look, I’m an American just like you. My motivation is to be happy and successful and to live the best life I can. And like most of you, I also want to make money and be rich. Richer than I am today. A big part of how I do that is by running seminars like this. But as much as I want to get richer, even more than that, I like helping people. And I know that I can teach you things that will help you, and that is worth much more than the entry fee.

It was a great example of the power of authenticity—of speaking honestly and from the heart. His candid admission of his own self-interest convinced me to give him the benefit of the doubt.

Practical > Theory

As Theodore Roosevelt told an audience in Paris in 1910, “It is not the critic who counts; not the man who points out how the strong man stumbles, or where the doer of deeds could have done them better. The credit belongs to the man who is actually in the arena, whose face is marred by dust and sweat and blood.”

Don't read books to sound intelligent at dinner parties; read books for mining useful ideas to implement in your life

A Single Most Important Secret Of Guy Spier

What I’m about to tell you may be the single most important secret I’ve discovered in all my decades of studying and stumbling. If you truly apply this lesson, I’m certain that you will have a much better life, even if you ignore everything else I write.

I sat down at my desk and actively imagined that I was Buffett. I imagined what the first thing would be that he would do. The minute I started mirroring Buffett, my life changed. It was as if I had tuned in to a different frequency. My behavior shifted, and I was no longer stuck.

So how can you apply these insights? We all know that mentoring is a big deal. Students and young professionals are often told to seek out mentors, just as those of us who are further along are supposed to find people to mentor. That’s all well and good if your heroes are accessible. Mine wasn’t. Buffett wasn’t sitting in his office in Omaha waiting for a call from this tainted graduate of D. H. Blair. Thankfully, this didn’t matter. I could get many— if not all— of the benefits of having him as a mentor by studying him relentlessly, and then imagining what he would have done in my shoes.

Imagining that I was Buffett, I also began to study the companies in his portfolio, wanting to see them through his eyes and to understand why he owned them. So I ordered up the annual reports for his major holdings, including CocaCola, Capital Cities/ ABC, American Express, and Gillette. This again gave me that uncanny feeling that Warren— and perhaps God Himself— was smiling at me.

Cashflow Statment > P&L Statment

vividly remember reading the report for Capital Cities/ ABC. Until then, I had never looked closely at the accounts of such a successful media company. When I saw the cash-flow statement, I found it hard to believe my eyes. The company was swimming in cash, and the income statement didn’t come close to conveying the might of this cash-generating machine. Most of the companies I’d analyzed as an investment banker were either hemorrhaging cash or grossly overstating their cash-generating ability. It felt as if I were embarking on a second MBA.

Diversification or Concentration

Warren Buffett, quoting Henry Ford, often talks about the importance of keeping all your eggs in one basket, then watch that basket very carefully. One thing that appalled me and that I’d seen too many times was the Wall Street practice of having many eggs in many baskets. Even the most reputable mutual fund companies have a practice of selling multiple funds. The ones that do well are those that then get the marketing dollars and raise more money from investors. The ones that do poorly are either shut down or merged into the better-performing funds. In the process, the failures are buried as if they’d never existed while the successes are highlighted.

inaction and patience are almost always the wisest options for investors in the stock market. (Inaction and patience are the ultimate drivers of success)

Surround yourself with Like-Minded

There are plenty of things I regret about that period in New York. But I made one decision that would prove hugely beneficial: I began to surround myself with a“ mastermind” group of investors who would become life-long friends and trusted sounding boards. It’s difficult, if not impossible, to become successful on your own. The greatest opera stars have singing teachers; Roger Federer has a coach, and Buffett meets regularly with like-minded people.

While others got caught up in the tech bubble of the late 1990s, I didn’t get lured in at all, partly because I was in the orbit of cool-headed investors like Buffett, Ruane Cunniff, and Tweedy, Browne. Their common sense helped to protect me from tech fever. This proved once again that environment trumps intellect.

Envy

Buffett and Munger joke that envy is the only one of the seven deadly sins that aren’t any fun.“ Envy is crazy,” remarks Munger.“ It’s 100 percent destructive. . . . If you get those things out of your life early, life works a lot better.”

Envy is also an emotion that we deny at our peril. In the financial markets, envy is a silent killer: it leads people to behave in ways they wouldn’t if they were more honest with themselves. For example, investors see their friends make a killing off tech stocks that are crazily overvalued, and they plunge in right before the bubble bursts. It’s important to be aware of these emotional forces bubbling inside us since they fundamentally skew our judgment, messing with our ability to make rational decisions. As an ancient rabbinical saying puts it: “Who is strong? He who masters his own passions.”

Often, we focus our analytical efforts in the wrong direction and miss something vital. So it’s crucial to be open to the possibility that we might be mistaken.

In my experience, it’s karmically better to focus on the positive and act as a force for good instead of getting gratuitously embroiled in acrimonious battles.

Charlie Munger :)

Mohnish Pabrai, who has spent time with him, later told me that Charlie is the smartest guy he’s ever met— even smarter than Buffett. What’s more,

Heard Behaviour (Misjudements)

Munger also explained that there’s a“ lollapalooza effect” when several forms of misjudgment occur simultaneously. For instance, when an investor sees friends and relatives making a fortune off Internet stocks, it provides “social proof” that these investments are a great bet since 10,000 lemmings surely can’t be wrong.

It’s difficult for professional investors, not just for amateurs who are new to the market, to resist this kind of lollapalooza of mind-bending distortions. We like to think we’re immune, but these forces are so powerful that they constantly subvert our judgment. And these are just a couple of examples of the kind of misjudgments that trip us up. In reality, there are many more, often occurring simultaneously.

Munger helped me to understand these tricks that the mind plays on us, and I began to see these patterns all around me.

Influence: The Psychology of Persuasion

I’d hang out in the lobby and watch with fascination as his eclectic group of guests passed by— people like Bill Gates, Ajit Jain, and Robert Cialdini. This reinforced my sense of Cialdini’s importance, so I read and reread his books multiple times, consciously pounding in his message over and over.

Why You Should Start to Write

At first, my letter-writing experiment was quite calculated, since I did it with an explicit desire to improve my business. I had a clear expectation of what the results would be. But it started to feel really good, and I became addicted to the positive emotions that this activity stirred in me. As I looked for more opportunities to thank people, I found that I truly did become more thankful. And the more I expressed goodwill, the more I began to feel it. There was something magical about this process of getting outside myself and focusing on other people.

Excerpts and Learning from Articles/Blogs

10 Key Learnings from One Upon the Wall Street by Peter Lynch! in the Indian context

phases in the markets are temporary, what really counts is the longevity and the earnings of the underlying business.

How the cycle of identifying the emerging businesses looks like:

1. The earnings explode and the ROCE expands.

2. There is skepticism and doubt about the business sustaining the numbers.

3. Earnings explode further.

4. Whatever doubt that was left gets taken care of and the business gets re-rated by the markets.

It's better not to chase the rising stock or a stagnant stock until the visibility of the next 3 years of earnings and ROCE direction isn’t clear.

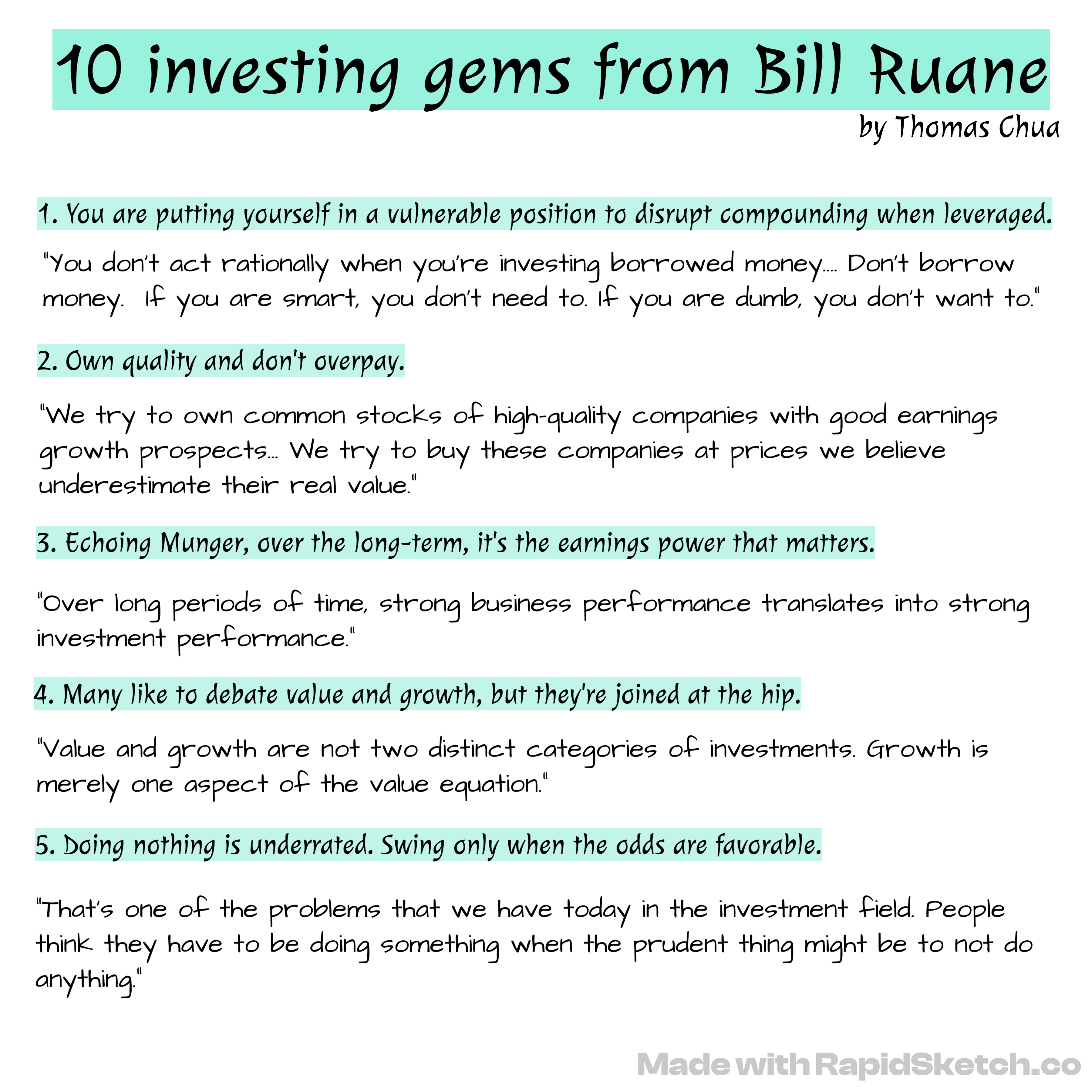

10 investing lessons from Bill Ruane:

When Warren Buffett closed his partnership in 1969, He recommended them to the one and only: Bill Ruane of Sequoia Fund to his investors who were looking to invest in a value fund after closing the partnership.

Bill Miller on market

The important point to keep in mind is both exercises are just guesses. No one has privileged access to the future, a future that involves what Keynes called irreducible uncertainty. No one knows how long the war in Ukraine will last nor what its outcome will be. No one knows how high inflation will go nor when it will begin to subside. No one knows if oil prices will stay over $100 or begin to decline or even double from here. No one knows how many times the Federal Reserve will raise rates nor what impact, if any, reducing its balance sheet will have on the economy.

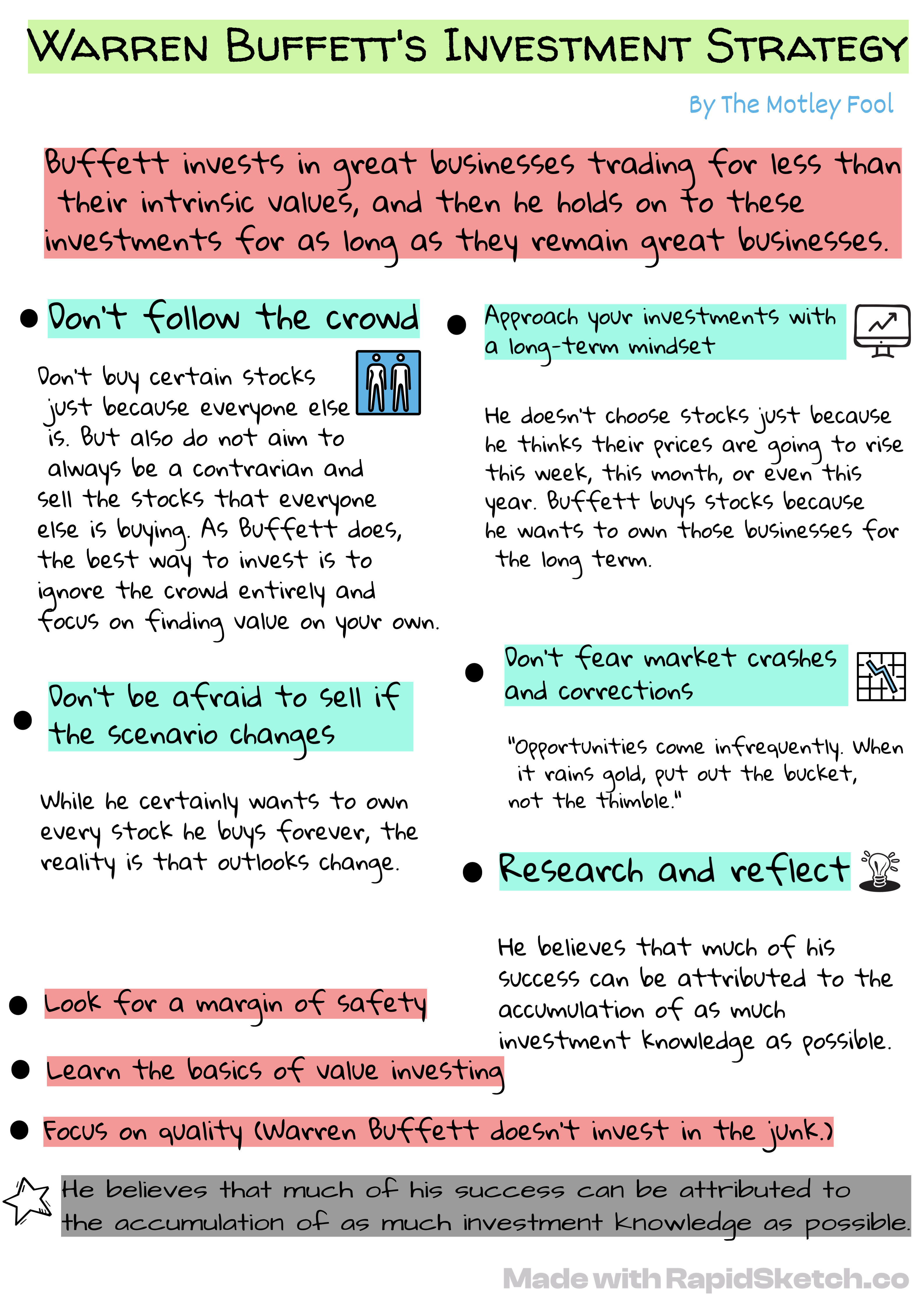

Warren Buffett's Investment Strategy

Prepared this sketch note from the article, Let me know your feedback on this :)

Bull and Bear market – same business, different narratives

Small Video Clips

Why you shouldn't worry about oil, rather your focus should be on Capable management and Growth prospects 10:32 to 12:07

Ajay Srivatsava View on Financials (3 Main Risk) 12:15 to 15:05

The choice is not really between value and growth but between value today and value tomorrow 14:49 to 31:28

The Intelligent Investor Approach to market 38:21 to 43:40

Why investing in a bear market is tough and why you should invest during a bear market 59:10 to 01:01:46

Concentration vs Diversification(Survival) 01:09:53 to 01:10:41

How to apply a margin of safety concept in the new-age listed business 01:11:19 to 01:14:29

Why you should say BIG NO to Crypto, A Brilliantly explained by Anurag Singh 26:08 to 29:05

All about New-Age IPO, Complete different view of IPO (How Companies Market Narratives) 34:20 to 42:49

Brilliant Write up as usual. Reading your content is always insightful. Thank you, please keep up the good work