We Don't Beat The Market, The Market Beats Us. (Investor Psychology & Behavioral Finance)

We Don't Beat The Market, The Market Beats Us. (Investor Psychology & Behavioral Finance)

Premium Issue - 14

Hi, Welcome to the 14th Special Edition

Brief Overview of What We will cover in this Issue

Detailed Key Takeaways from the book I am reading Currently

6+ Decent Articles to read and Key Takeaways from them.

Value vs Quality vs Momentum

Mistakes to avoid in smallcap Investing (Video Clip)

Understanding Market Cycle (Video Clips from FM)

I Publish only 4-5 quality Posts per month (2 Free, 2 Paid) so be assured that I take care in adding value to my free subscribers as well as paid ones. Do not unsubscribe in anticipation of the only paid newsletter :), will send a Free post Next Saturday

If you want to read the full issue, Do Subscribe to Paid Plan (If there is any error do subscribe it by paying Here and send a mail id and Payment screenshot on Twitter DM)

(Note: Gmail will truncate emails that are more than 102KB so please prefer to read a direct post from Our Blog to avoid missing some of the last section of content)

Investing: The Last Liberal Art (Part-3)

You may be asking yourself if the discounted present value of future cash flows is the immutable law for determining value, why do investors rely on relative valuation factors and second-order models? Because predicting a company’s future cash flows is so very difficult.

when it comes to money, people are not consistently reasonable or knowledgeable. We also know that subjective probabilities can contain a high degree of personal bias. Any time subjective probabilities are in use, it is important to remember the behavioral finance missteps we are prone to make and the personal biases to which we are susceptible.

William Poundstone further popularized the Kelly criterion in his popular book, Fortune’s Formula: The Untold Story of the Scientific Betting System That Beat the Casinos and Wall Street (2005).

The stock market is more complex than a game of blackjack, in which there is a finite number of cards and therefore a limited number of possible outcomes. The stock market has thousands of companies and millions of investors and thus a greater number of possible outcomes. Using the Kelly approach, in conjunction with the Bayes theorem, requires constant recalculations of the probability statement and adjustments to the investment process. Because in the stock market we are dealing with probabilities that are less than 100 percent, there is always the possibility of realizing a loss. Under the Kelly method, if you calculated a 60 percent chance of winning you would bet 20 percent of your assets, even though there is a 2 in 5 chance of losing. It could happen.

Two caveats to the Kelly criterion that are often overlooked: You need (1) an unlimited bankroll and (2) an infinite time horizon. Of course, no investor has either, so we need to modify the Kelly approach. Again, the solution is mathematical in the form of simple arithmetic.

Put differently, investors need to understand the difference between the average return of the stock market and the performance variation of individual stocks. One of the easiest ways for investors to appreciate the differences is to study sideways markets.

Most investors have experienced two types of stock markets—bull and bear—that go either up or down over time. But there is a third, less familiar type of market. It is called a “sidewinder” and it produces a sideways market— one that barely changes over time.

When I first heard that argument—that we might be facing a sideways market similar to the late 1970s and it was best to avoid stocks— I was puzzled. Was it really true that sideways markets are unprofitable for long-term investors? Warren Buffett, for one, had generated excellent returns during the period; so did his friend and Columbia University classmate Bill Ruane. From 1975 through 1982, Buffett generated a cumulative total return of 676 percent at Berkshire Hathaway; Ruane and his Sequoia Fund partner Rick Cunniff posted a 415 percent cumulative return. How did they manage these outstanding returns in a market that went nowhere? I decided to dig a little. First, I examined the return performance of the 500 largest stocks in the market between 1975 and 1982. I was specifically looking for stocks that had produced outsized gains for shareholders. Over the 8-year period, only 3 percent of the 500 stocks went up in price by at least 100 percent in any one year. When I extended the holding period to 3 years, the results were more encouraging: Over rolling 3-year periods, 18.6 percent of the stocks, on average, doubled. That equals 93 out of 500. Then I extended the holding period to 5 years. Here the returns were eye-popping. On average, an astonishing 38 percent of the stocks went up 100 percent or more; that’s 190 out of 500.14

Putting it in Gould’s terms, investors who observed the stock market between 1975 and 1982 and focused on the market average came to the wrong conclusion. They wrongly assumed that the direction of the market was sideways, when in fact the variation within the market was dramatic and led to plenty of opportunities to earn high excess returns. Gould tells us “the old Platonic strategy of abstracting the full house as a single figure (an average) and then tracing the pathway of this single figure through time, usually leads to error and confusion.”

it suggests that very high or very low performance is not likely to continue and will probably reverse in a later period. (That’s why it is sometimes called reversion to the mean.)

J. P. Morgan was once asked what the stock market would do next. His response: “It will fluctuate.” No one at the time thought this was a backhanded way of describing regression to the mean. But this now-famous reply has become the credo for contrarian investors. They would tell you greed forces stock prices to move higher and higher from intrinsic value, just as fear forces prices lower and lower from intrinsic value, until regression to the mean takes over. Eventually, a variance will be corrected in the system.

The frustration comes from three sources. First, reversion to the mean is not always instantaneous. Overvaluation and undervaluation can persist for a period longer— much longer— than patient rationality might dictate.

Yesterday’s normal is not tomorrow’s. The mean may have shifted to a new location.

Up until the 1950s, the dividend yield on common stocks was always higher than the yield on government bonds. That’s because the generation that lived through the 1929 stock market crash and Great Depression demanded safety in the form of higher dividends if they were to purchase stocks over bonds.

Uncertainty is different. With uncertainty, we don’t know the outcome, but we also don’t know what the underlying distribution looks like, and that’s a bigger problem. Knightian uncertainty is both immeasurable and impossible to calculate. There is only one constant: surprise.

The attack on Pearl Harbor in 1941 and the 9/ 11 terrorist attack on the World Trade Center are examples of black swan events. Both were outside the realm of expectation, both had an extreme impact, and both were readily explainable after the fact.

According to Tetlock, “How do you think matters more than what you think?” It appears experts are penalized, like the rest of us, by thinking deficiencies. Specifically, experts suffer from overconfidence, hindsight bias, belief system defenses, and lack of a Bayesian process. You may remember these mental errors from our chapter on psychology. Such psychological biases are what penalize System 1 thinking. We rush to make an intuitive decision, not recognizing that our thinking errors are caused by our inherent biases and heuristics. It is only by tapping into our System 2 thinking that we can double-check the susceptibility of our initial decisions.

When you analyze your portfolio, will you resist the almost uncontrollable urge to sell a losing position, knowing full well the angst you feel is an irrational bias— the pain of loss being twice as discomforting as the pleasure of an equal unit of gain? Will you stop yourself from looking at your price positions day in and day out, knowing that the frequency with which you do is working against your better judgment? Or will you bow down to your first instinct and sell first and ask questions later?

When thinking about companies, markets, and economies, will you rest with your first description of events? Knowing that more than one description is possible and the dominant description is most often determined by the extent of media coverage, will you dig deeper to uncover additional, perhaps more appropriate, descriptions? Yes, it takes mental energy to do this. Yes, it will take more time to reach a decision. Yes, this is more difficult than defaulting to your first intuition.

One critical difference between building a model of a log cabin and building a model of market behavior is that our investing model must be dynamic. It must have the ability to change as the circumstances change. As we have already discovered, the building blocks of fifty years ago are no longer relevant because the market, like a biological organism, has evolved. A model that changes shape as its environment changes may be difficult to envision. To get a sense of how that could work, imagine a flight simulator. The great advantage of a simulator is that it allows pilots to train and perfect their skills under different scenarios without the risk of actually crashing the plane. Pilots learn to fly at night, in bad weather, or when the plane is experiencing mechanical difficulties. Each time they perform a simulation, they must construct a different flight model that will allow them to fly and land safely. Each one of those models may contain similar building blocks but assemble in a different sequence; the pilot is learning which building blocks to emphasize for each of the scenarios.

The pilot is also learning to recognize patterns and extrapolate information from them to make decisions. When a certain set of conditions presents itself, the pilot must be able to recognize an underlying pattern and to pull from it a useful idea. The pilot’s mental process goes something like this: I haven’t seen this exact situation before, but I saw something like it, and I know what worked in the earlier case, so I’ll start there and modify it as I go along.

Building an effective model for investing is very similar to operating a flight simulator. Because we know the environment is going to change continually, we must be in a position to shift the building blocks to construct different models. Pragmatically speaking, we are searching for the right combination of building blocks that best describes the current environment. Ultimately, when you have discovered the right building blocks for each scenario, you have built up experiences that in turn enable you to recognize patterns and make the correct decisions.

Students at the Wharton School will have spent a great deal of time studying the theory and structure of financial markets, but what additional insights could they have learned by taking Social Problems and Public Policy, Technology and Society, Sociology at Work, or Social Stratification?

To be a successful investor, you need not spend four years studying sociology, but even a few courses in this discipline would increase the awareness of how various systems organize, operate, thrive, fail, and then reorganize.

Watching the students pass one by one on their way to classes in their chosen major, I can’t help but wonder where they will all be in twenty-five years. Will their college education have adequately prepared them to compete at the highest level? Once they reach retirement age, will they be able to look back and measure their life’s work as a success or will they see it as something less than that?

The lesson we are taking away from this book is that the descriptions based solely on finance theories are not enough to explain the behavior of markets.

Over the years we have increased our baskets of knowledge, but what is surely missing today is wisdom. Our institutions of higher learning may separate knowledge into categories, but wisdom is what unites them. Those who make an effort to acquire worldly wisdom are beneficiaries of a special gift. Scientists at the Santa Fe Institute call it emergence. Charlie Munger calls it the lollapalooza effect: the extra turbocharge that comes when basic concepts combine and move in the same direction, reinforcing each other’s fundamental truths. But whatever you decide to call it, this broad-based understanding is the foundation of worldly wisdom.

The Behavior Gap: Simple Ways to Stop Doing Dumb Things with Money (Part-1)

This is a book about how you can make good money decisions. The author is not talking about which investment to buy or how much to invest in the stock market. He is talking about decisions that are in tune with reality, with your goal, and with your value.

This is also a book about how to avoid confusion, how to cope with fear, and how to stay grounded when making financial choices. That sounds hard— and as we’ll see, it’s not always easy. But it’s pretty simple. In fact, simplicity is one of the keys.

No plan will cover every situation— and that’s okay.

You don’t have to choose the perfect investment or save exactly the right amount or predict your rate of return or spend hours watching television shows about the stock market or surfing the Internet for stock picks. You don’t need a plan for every contingency. So if planning isn’t the solution to our money problems, what is? More simply, what can we do to get what we really want? We can stop chasing fantasies. We are not going to get what we want by beating the market or picking the perfect investment or designing the perfect bulletproof financial plan. In fact, when we try to do those things we get into big trouble. We can protect ourselves— to a point. Risk is what’s left when you think you’ve thought of everything.

Our assumptions about the future are almost always wrong. We can never think of everything— but we can take sensible steps to protect ourselves from life’s inevitable surprises. We can embrace uncertainty. Change isn’t always a problem. Many— perhaps most— of life’s surprises are good news. If we aren’t locked down into a rigid plan, we can recognize and seize opportunities when they come up. We can decide what we really want.

When someone asks you what you really want out of life, you’re probably not going to say you want an investment that delivers good returns. Like the rest of us, you want to be happy and fulfilled.

Once you know what you (and your family) really want, you will know what to do— how much insurance to buy, where to invest your money, and whether to quit your job and start a new venture. We can make decisions that make sense. We can’t control the markets or the economy, but our behavior is up to us. It’s true that the outcomes of our decisions may vary. In fact, you can make a good decision and have a bad outcome. But sensible, reality-based choices are our best shot at reaching our goals.

We can trust our luck. Most financial planners don’t like to talk about luck. The idea that some things just happen by chance can be a scary one.

One of those lessons is that you aren’t in charge of everything. Do what you can, and then relax.

I stood by what really mattered to me— I wanted Sundays off— and I lost my job. What a disaster, right? And so far, at least, that decision— and that disaster— have made all the difference.

I don’t believe that there is a secret to getting rich. But in the end, financial decisions aren’t about getting rich. They’re about getting what you want— getting happy. And if there is a secret to getting happy, it’s this: be true to yourself. Maybe you’ve heard that one before. But I’ll bet you haven’t read it in a book about money.

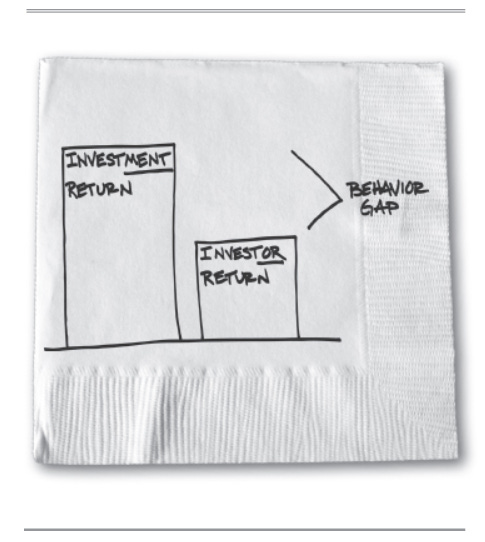

WE DON’T BEAT THE MARKET, THE MARKET BEATS US

Typically, the studies find that the returns investors have earned over time are much lower than the returns of the average investment.

What that means is that we’re leaving money on the table. Take mutual funds. All we had to do was simply put our money in an average stock mutual fund and let it sit there. But most investors didn’t do that. Instead, they moved their money in and out of stock funds. Their timing was miserable— and it cost them dearly.

It’s clear that buying even an average mutual fund and holding on to it for a long time has been a pretty decent strategy. But real people don’t invest that way. We trade. We watch CNBC and listen to Jim Cramer yell.

We buy what’s up and sell what’s down. In other words, we do exactly what we all know we shouldn’t do.

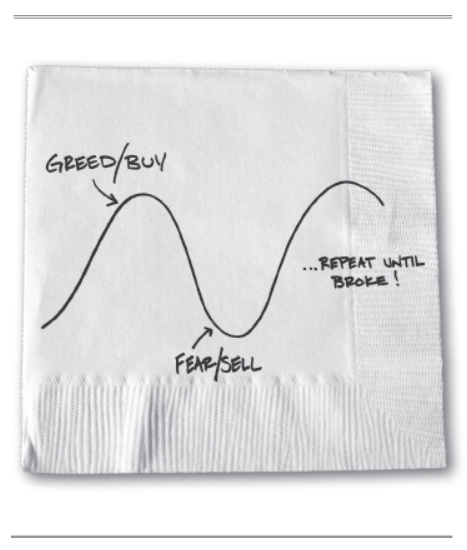

But if you think we get irrational at market tops, wait until you see how we behave at market bottoms. October 2002 was the fifth month in a row that investors pulled more money out of stock mutual funds than they put into them— the first time ever such a streak had occurred.

Stop and think about this for a second. At the market peak, we were borrowing against our homes to buy over-priced technology stocks. At the bottom, we couldn’t sell stocks fast enough. And where was all the money going? Investors were using it to buy bond funds, which recorded record cash inflows during the period— even though bond prices were by some measures higher than they’d been in more than forty years. This is nothing new. We do it all the time. We did it with emerging markets in 2004, and with real estate in 2006 and 2007… Repeat until broke. No wonder most people are unsatisfied with their investing experience.

The more expensive stocks (or houses) are, the more risky they are— yet that’s when we tend to find them most attractive. In short, investors as a group tend to be horrendously bad at timing the market.

It’s not that we’re dumb. We’re wired to avoid pain and pursue pleasure and security. It feels right to sell when everyone around us is scared and buy when everyone feels great. It may feel right. But it’s not rational.

Excerpts and Learning from Articles/Blogs

Investment Stories vs. Facts (Must Read)

"Most stock-picking stories, advice, and recommendations are completely worthless." Ed Thorp

"Stories are more powerful than statistics because the most believable thing in the world is whatever takes the least amount of effort to contextualize your own life experiences." Morgan Housel

Don’t let urban myth dictate your investment activities. And whatever you do, look for evidence where stories are based on a sample size of one

Compounding Indefinitely

When people wonder about Warren Buffett buying railroads and utilities earning 10-11% returns on incremental invested capital, they need to remember the table above and consider whether Buffett bought these businesses because of (1) long runways for growth and reinvestment and (2) predictable compounding for decades, with the return benefits becoming more pronounced every year: a 23-bagger in 30 years if returns on incremental invested capital are 11%, and a 30-bagger in 30 years if returns improve to 12%. When a company can reinvest retained earnings at attractive rates over long time periods, patient shareholders can defer taxes indefinitely and reap the full benefits of compounding.

We Need To Retire More Often

We are constantly searching for dopamine hits in bad neighborhoods. Temporary pleasure increases desire, never resulting in the goal of lasting happiness.

Wealth and wrong choices make the outcomes worse.

Viktor Frankl sagely points this out. When people can’t find a deep sense of meaning, they distract themselves with pleasure.

The stock market is a terrible place to find refuge. The shorter the time frame, the worse the outcome.

Determining happiness using the market’s daily movements provides a coin’s flip chance of fulfillment.

A properly constructed financial plan provides such a haven. A real financial plan is built based upon the only factor we can rely on – change.

Carl Richards gets it. Financial plans should be written in pencil, not carved in stone.

Find comfort in change, not wealth.

Create a plan that fits your lifestyle, not an outdated relic of the past.

Wealth vs. Getting Wealthier

For a lot of people, the process of becoming wealthier feels better than having wealth.

U.S. household net worth is $80 trillion higher today than it was ten years ago, which is astounding. But it’s about $700 billion lower than it was three months ago, which is honestly nothing. Yet one of those figures creates ten times the headlines, ten times the attention, ten times the emotions, ten times the introspection. It has nothing to do with the level of wealth and everything to do with the trajectory.

The reason markets can go up a lot, in the long run, is because they make you pay the cost of admission of going down a lot in the short run.

An addiction to the process of making money is a version of never having enough and never being satiated. It’s a game that can’t be won but offers the illusion of a finish line right around the corner.

Acceptance of the process, knowing it’ll be a constant chain of surprises, volatility, setback, and disappointment, but if you can stick around long enough the odds of eventual growth and success are in your favor.

Money buys happiness in the same way drugs bring pleasure: Incredible if done right, dangerous if used to mask weakness, and disastrous when no amount is ever enough.

Investing Learning from Seth Klarman Interview

Value vs Quality vs Momentum

Access Q4FY22 Notes and comprehensive notes of the last 9 quarters about Indian Companies (Made by Smart Sync) Around 20 Various Sector Covered

Small Video Clips

When you should “consider” selling your long-term stocks (2:50 to 3:31)

How Salaried people can Balance time between job and investment (Part-time investing can be done?) (4:00 to 6:14)

Joel Greenblatt's Magic Formula and How you can apply it in Indian Stocks

Finding a Perfect Small cap company is next to impossible what should you check and what you should avoid while buying smallcap companies (17:10 to 23:50)

Mistakes to avoid in smallcap Investing (45:11 To 49:52)

Understanding Market Cycle (Viraj Mehta) (02:35 to 8:00)

Sector Vise Valuation Comparison with Nifty50 (13:45 to 19:15)

How to gauge corporate governance in smallcap companies (55:08 to 56:23)

Why your money lessons to your kids will not work and why you shouldn't teach them about money at a very younger age (19:48 to 21:32)