#065: "The complete guide to researching businesses fundamentally",

What really Matters for Investing, Getting Wealthy Vs Staying Wealthy

Hi, Welcome to the 65th Edition

Brief Overview of What We will cover in this Issue

Detailed Key Takeaways from the book I am reading Currently

Getting Wealthy Vs Staying Wealthy

Uncovering the 5 factors for Multi-Bagger returns

What Really Matters for Investing

Lessons on investing from two renowned investors (Video Clips)

How to eliminate bad decisions using a mental model (Video Clips)

Since I ended my paid subscription, I need your support now if you find my efforts of curating investing insights worthy of it. You can Extend your support by ensuring shopping on Amazon through my affiliate links whenever you shop :) Also can support by paying any amount to buy Best Free Investing E-books

You can also voluntarily upgrade your free subscription to a paid one if you think it is valuable

The Investment Checklist (Part-1)

Too often, investors buy stocks by relying on recommendations from other investors, or on hunches, or because of isolated facts they’ve heard or read about a business. When you make your purchase decisions on these factors and do not take the time to thoroughly understand the businesses you are buying, you’re more prone to make investment mistakes. Your decision-making then becomes dangerous because you don’t really know enough, and you’re relying on other people and the information (or misinformation) they provide about a particular stock.

Instead, your investment purchases should be based on understanding the value of a business through in-depth research. If you truly understand the value of a business, then you will be in a position to recognize investment opportunities and can more easily make buy or sell decisions.

For example, think about any major purchase you’ve made in your life— whether it’s a house, or a car, or an expensive piece of jewelry or electronics. Before you spent all that money on whatever it was, you probably spent some time researching to make sure your money would be well spent.

The more you know about your purchase, the more easily you will be able to recognize a good deal. The same is true when buying or selling a stock. The more you understand the dynamics of a business and the people operating it, the better the odds that you will be able to recognize a good deal on a business.

My instinct after failing to find a good investing framework was to over-research potential investments. I often ended up reading everything I could get my hands on about a potential investment. As a result, I subjected myself to information overload and was unable to recognize good information. I also kept repeating investment mistakes, such as paying too much for a business or partnering with the wrong management team.

I set out to establish a systematic process to force me to think through my investment ideas more carefully and help me avoid repeating the same investment mistakes. Over the past 10 years, I began to use checklists of questions I needed to answer to make informed investment decisions— questions that would guide me in learning about a business’s competitive position, customer positioning, and management strength. To come up with the questions, I studied the past mistakes I had made investing, and I read many books about the common mistakes made by investors and executives.

The Investment Checklist is for anyone who’s investing in stocks, at any level— if you’re just starting out and thinking about what you want to invest in, or if you already have a portfolio (of any size) that you want to manage better and watch your money grow (after all, no-one wants to watch their investments lose money, shrink, or disappear altogether!). This book is for anyone who wants to learn how to value a business and invest for the long term

Do you check stock prices frequently?

Do falling stock prices make your stomach churn?

Do you react quickly to positive or negative news announcements about the companies whose stock you own?

Do you ever feel you’re under time pressure to make buy or sell decisions?

Do you have a high portfolio turnover? Are you buying and selling shares often?

Do you feel you need to defend your investments when others challenge you?

If you answered “yes” to any of the above questions, this book can help you make better investment decisions, by helping you research more effectively so you’ll truly understand how a business operates and is managed.

This book tells you what information you really need and where to find it. The majority of the questions can be answered with information that is relatively easy to find.

Researching a business over a long period of time allows us to sort through things rationally and puts us in a position to better interpret information.

The checklist is useful for compiling information that goes against your investment thesis. It is human nature to overweight information that supports your investment thesis and underweight information that is contrary to your investment thesis.

Knowing when to sell an investment is one of the most difficult decisions you have to make. Most sell decisions are based on judgment, feel, or instinct.

The checklist helps you learn when to sell by helping you identify when the fundamentals of a business, such as the quality of the business or management team, begin to change.

How to Generate Investment Ideas

There are many ways you can generate investment ideas, some qualitative, and some quantitative.

Quantitative methods include looking at specific financial or operating metrics, whereas qualitative methods rely on more subjective characteristics, such as management strength, corporate culture, or competitive advantages.

This chapter explores why stocks become undervalued, how to generate investment ideas, how to filter these ideas, and how to keep track of them. These steps are critical to creating a pool of stock ideas. How Investment Opportunities Are Created

you need to be patient, and you have to be ready for the right opportunities. It is important to understand that good investment idea are rare, and consistent success in the stock market is elusive.

Most investors are far too optimistic: They often think they’ve found great ideas when they haven’t.

In contrast, investors with the best long-term track records have made most of their money with just a handful of investment ideas.

To learn which area of the stock market is in the greatest distress, look for those areas where capital is scarce. The scarcity of capital creates less competition for assets, which decreases prices. Ask yourself, what areas of the stock market are investors fleeing, and why?

Most stock price drops are due to some type of uncertainty about the business, and there are many possible reasons:

In most of these cases, investors automatically assume the worst-case scenario and tend to sell stocks first and ask questions later. Once the reality starts to set in that the ultimate outcome will not be as bad as expected, then stock prices adjust and typically rise.

Ideally, you want to identify those areas where the outlook is most pessimistic and identify whether the sources of pessimism are temporary or permanent.

Be Wary of Exciting New Trends that Turn out to Be Fads

You must also learn to identify those areas of the stock market that are benefiting from abundant sources of capital, which drives up prices, so you can be careful investing in them. Wall Street is good at pitching stories, and investors tend to get excited by what they believe is an important new trend. However, many of these exciting major trends turn out to be fads that are based on speculation, rather than fundamentals.

How to Spot Investment Bubbles

To understand where current bubbles exist, ask, “Where is a lot of money being made very quickly?” Look at the Forbes magazine list of billionaires. What industries are the new billionaires coming from?

When capital is abundant, it searches for other similar businesses to duplicate success. The IPOs of technology businesses caused many other technology businesses to be formed and seek to go public. Here are a few signs of a bubble:

Lots of available capital

Higher levels of leverage

Decreased discipline from lenders as they try to get higher returns than through conventional lending guidelines

Decreased responsibility for the borrower, combining high leverage and looser lending terms

Using Stock Screens

There are many different types of screening tools available.

For example, if you are looking at a multiple of last year’s earnings, this can be misleading if the company reported a big loss in the prior year. Investors often need to adjust GAAP earnings to understand the real earnings of a business.

For example, in 2006 and 2007, the average trailing 12-month P/ E for retailer 99 Cent Only Stores was more than 90 times. After adjusting the earnings for special charges 99 Cent Only Stores took in those two years, I learned that the adjusted P/ E was closer to 12 times rather than the 90 times being reported.

On a standard stock screen, many of my best investments showed up as having a P/ E ratio of more than 50 times because GAAP accounted for such factors as restructuring costs that reduced earnings. After I made GAAP adjustments, I found that these ostensibly high P/E ratio businesses were really trading at only five times earnings, not 50. Had I relied exclusively on stock screens, I would have missed many of my best investments.

Keeping an Eye on New-Lows Lists

Paul Sonkin, manager of the Hummingbird Value Fund (a microcap fund), uses stock screens and new-lows lists, but he believes these tools are misused by investors 99 percent of the time. According to Sonkin, “A lot of investors will put together a screen of low price-to-book or low price-to-earnings stocks, but usually, 90 percent of the companies on the screen are cheap for a good reason. Many stay on these lists for a long time.” Sonkin believes the proper way to use a screen or new-lows list is to run them on a weekly basis and look for new companies that appear on the list. This way, you are able to separate the companies that deserve to be there from those that may only be suffering from a temporary problem.

Reading Newsletters, Alert Services, Online Recommendations, and Media Recommendations

There are many publications that tout stocks. It is better to stick to those services that are fact-based,

Rather than those services that are more interested in selling subscriptions by marketing high rates of returns to their subscribers. Fact-based publications are those where no opinion is attached and instead corporate events are chronicled. Be aware of self-serving recommendations and less-than-transparent presentations of results.

Following Other Investment Managers

Many investors (professionals included) generate ideas by closely tracking the holdings of well-known investment managers with above-average track records.

These are usually investors who have had recent success, so the media constantly reports their new holdings.

The problem with following others is that most of these great records were generated by past investments, and investors wrongly conclude that existing and future investments will have similar results.

When the filings came out, I would be excited to discover that the investment managers I admired had made some new investments or significantly increased their position in a stock. If it was an investment idea I understood, this excitement translated into higher conviction, sometimes causing me to cut corners on my own research.

There are several disadvantages to following other investment managers: Most great investment track records come from a limited number of investments. For every investment, a successful investment manager makes, only one will appreciate substantially, contributing outsize returns to the investment record, while the others will either mildly perform or underperform.

You typically will not know the reason why a certain investment manager is buying or selling a stock. Perhaps the investment manager is suffering from investment redemptions and he or she needs to sell stocks.

No matter how good they are, all investment managers will make mistakes, and you may be following them into such a mistake.

Therefore, in the end, be careful about following the ideas of other investors.

Casually Reading the Business Press

The best investment ideas usually come from those businesses that are in distress. Focus on those articles that are not success stories but those about distress, to give you better odds of finding a well-priced investment.

Buying Shares to Track a Business

By purchasing a very small piece of a business, you’ve guaranteed that you will not forget the business and that you’ll have consistent reminders about that business.

Existing Portfolio

Don’t Ignore Your Existing Investment Portfolio Admittedly, it is more exciting to discover opportunities outside of your portfolio, but it’s not necessarily more beneficial.

Many investors forget to look at their existing portfolios for ideas.

Often, your best opportunities are right in front of you. If a stock you hold drops in price, this may represent the best investment opportunity for you,

For example, when the S& P 500 dropped 36 percent in 2008,

Instead of attempting to analyze many of the new opportunities being offered, my firm decided to analyze our own portfolio holdings that were trading at significantly lower prices than they had just weeks or months before.

Research Upcoming IPOs

You can regularly research IPOs, spin-offs, and stocks of companies that are exiting bankruptcy,

The biggest advantage of tracking these businesses is that there is no public price to influence you.

You can calculate a reasonable valuation range for the business in advance, and then compare your value to the business’s trading price.

For example, I analyzed the pediatric nutrition business Mead Johnson Nutrition before it was spun off from parent Bristol-Myers Squibb. Because there was not a public price to influence me, I determined that the stock was worth $ 40 per share and that I should buy it at any price below $ 30 per share. When the price of the spin-off was set at $ 27 per share in February 2009, I purchased the stock, which quickly increased to $ 43.70 at the end of 2009. Had I not prepared in advance, I would have missed this opportunity.

Criteria Is a Filter

Your criteria can be as simple as looking for a simplified business with a large market opportunity, managed by a great management team, and trading at a low price. You can also set criteria of what you do not want to invest in. For example, you may want to avoid businesses that have a high dependency on commodity resources, such as exploration and production (E& P) businesses, because oil prices are difficult to forecast.

You can list what your preferences are for a business, such as these:

A recurring revenue stream

A business with high organic growth prospects (i.e., growth that is not accomplished by acquiring or merging with other businesses)

Management that has a long tenure at the business

A competitive moat

Strong existing or potential financial characteristics, such as high free-cash-flow

High existing or potential returns on invested capital

Limited competition

Low capital-expenditure requirements

A diversified customer base

A strong balance sheet

Evaluating the business in each of these 10 areas will help you understand the tradeoffs you are making when investing in a particular business.

The more closely a business meets your stringent criteria, the less risk you are taking. For example, it is easier to monitor a business with limited competition rather than one that has a lot of competition. If a business meets only four or five of your criteria, you can usually pass on the business, as most investment mistakes are made when you stretch your criteria.

Once you add an investment to your list, you should begin learning about the business and management team, and track the valuation of the business using financial metrics such as free cash flow (FCF) yield or total enterprise value (TEV) to earnings before interest and taxes (EBIT) to alert you if a business drops in value. Because of the GAAP issues mentioned earlier, you may want to avoid using valuation metrics such as price-to-earnings ratios.

Valuation Is a Filter

The one thing you can’t fix after making an investment is the price you pay, so it is critical to remain disciplined on price.

Your future rate of return will be determined by the price you pay for the business.

The case study gives you an example of how investment manager Brad Leonard generated high returns for his investors by paying low prices.

Brad Leonard founded BML Capital Management, LLC in 2004. He has compounded capital at a rate of 26.94 percent, net after fees from 2004 to 2010, compared to 3.87 percent, net for the S& P 500.

He typically pays three times enterprise value (EV) to EBITDA for a stock, and he prefers to buy businesses that do not need a lot of capital expenditures to maintain their businesses and those that have little to no debt.

In 2009, when the stock market was declining, Leonard was buying stocks at one to two times EBITDA. Leonard says, “When you are paying one or two times EV EBITDA, not much needs to go right. If the business survives, you win. As long as the business does not end, you don’t need to make a lot of great assumptions in your analysis.

For example, Leonard first began buying Kirkland’s, a home décor retailer, at $1.70 per share in the fall of 2007. Shortly thereafter, the stock price declined to $ 0.70 per share (when the stock market declined by more than 36 percent in 2008). As Leonard was buying Kirkland’s, the fundamentals of the business continued to improve. After reporting negative comparable store sales in the fourth quarter of 2007, Kirkland’s same-store sales turned positive in the first two quarters of 2008. Cash flows, comparable store sales, and margins all continued to improve, yet the stock price continued to decline. Leonard stepped on the gas even more in his purchases. He said, “Every quarter, the results of Kirkland’s would improve, and it seemed that no one cared. At this time, I thought it was likely the company would post around $ 20 million in EBITDA, so in essence, I was buying the stock around 1 to 2 times EV to EBITDA.” The stock eventually recovered to around $ 2 per share by 2008, and by 2009, it was trading at more than $ 20 per share. Leonard’s disciplined buying was well rewarded.

How to Generate Investment Ideas Using a Spreadsheet to Track Potential and Existing Holdings

If you are comparing your existing holdings with hundreds of potential investment opportunities rather than a limited set, you increase the probability of making good investments and avoiding bad ones. The more comparisons you can make in your spreadsheet, the higher the probability of uncovering an investment idea. In addition, those comparisons will increase your awareness of areas of the stock market and individual stocks that are out of favor.

Gradually Building a Spreadsheet of Potential Investments When you do not have investment opportunities that you are ready to act on, you can use your time to prepare for future opportunities.

When you identify a unique business or superior management team, add the business to your inventory of ideas or watch list, regardless of its current valuation. This is the secret sauce to investing intelligently because it allows you to act decisively when a good opportunity is in front of you,

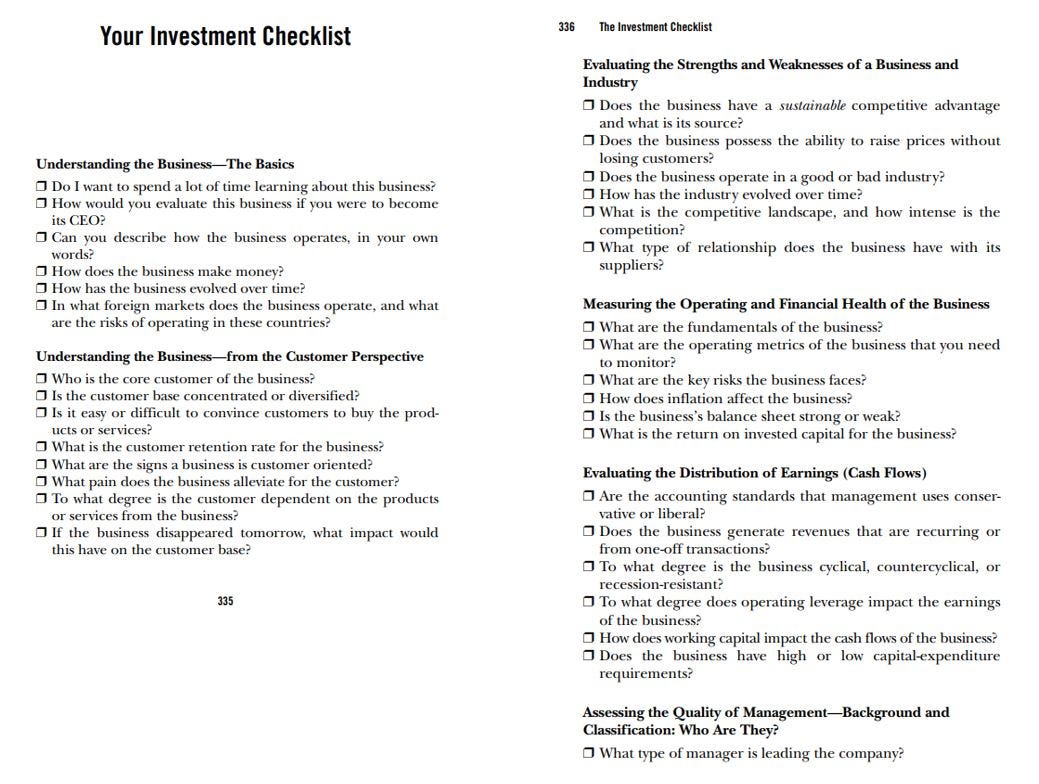

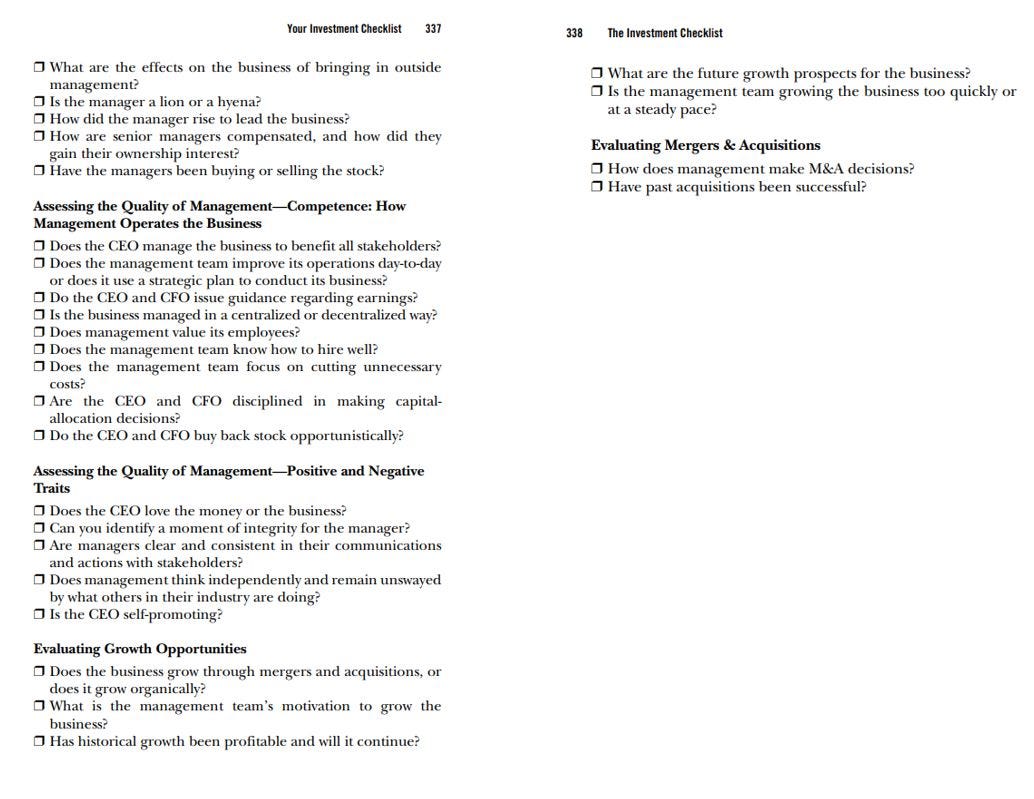

Understanding the Business— The Basics

Before you begin to analyze a business, ask yourself if you are interested in learning more about it. If not, you probably won’t have sufficient interest to do in-depth research and as a result, you may make an uninformed investment decision.

You can’t truly understand a business in a couple of weeks. It takes a long time, years in most cases, to truly understand how a business operates and to determine the competence and integrity of a management team.

It is a continuous process, and if your interest begins to wane in a couple of weeks, you will not have the stamina to continue to learn about the business over the long term.

If you are just beginning to invest, it is best for you to analyze one business over a long period of time. Too often, even professional analysts spend their time analyzing too many businesses, and they never develop the ability to fully understand the value of a business (i.e., they don’t see the whole picture).

If you find that it is extremely difficult for you to evaluate the business or that you are simply not interested, this is a sign you might want to pass on the investment.

Instead of over-investing in a process that yields less return, try to develop a deeper understanding of businesses you genuinely care about.

It is common sense that you are less likely to succeed at something you are not interested in, yet investors force themselves to study such businesses.

Personally liking a product or service can lead you to believe that others will like it as well. For example, it’s hard to objectively weigh criticism of your favorite restaurant: Because your own experience has been different, you may even discount a negative report.

Whether positive or negative, be aware that your personal preferences may negatively influence your investment decisions.

To understand how a business operates, read the business description found in the 10-K.

Each of the business’s segments

Distribution channels

Marketing strategies

Manufacturing activities

Regulatory requirements

Extensive management discussions of strategies and risks facing the business

Industry size and trends

Insight into the competitive environment

After reading this section carefully, write in your own words how the business operates. How does the business manufacture products or produce its services? How does it distribute these goods and services to the customer? Try to visualize how a product or service is delivered.

By writing it in your own words, you will gain a deeper understanding of how the business operates than you would by reading the text and taking light notes.

If you are having a difficult time understanding a business, ask what the customer’s world would look like without the product or service.

Another method you can use to simplify a business description is to find an analogy that best explains how the business operates.

How does the business make money?

At first glance, this sounds like a simple question to ask, but it is critical for you to summarize how a business generates earnings. If you can’t understand how a business makes money, then you should not invest in it.

Many investors fall into the trap of investing in businesses where they do not understand how the business generates earnings.

How has the business evolved over time?

A historical perspective on a business provides both a deeper understanding and useful insight into its competitive advantage. You can better understand if the success of the business is due to managerial brilliance or simply being at the right place at the right time.

Most businesses will include a timeline or history of how their business evolved.

1) Getting Wealthy vs. Staying Wealthy

Getting money is one thing. Keeping it is another.

If I had to summarize money success in a single word it would be “survival.”

Getting money requires taking risks, being optimistic, and putting yourself out there.

But keeping money requires the opposite of taking risk. It requires humility, and fear that what you’ve made can be taken away from you just as fast. It requires frugality and an acceptance that at least some of what you’ve made is attributable to luck, so past success can’t be relied upon to repeat indefinitely.

Michael Moritz, the billionaire head of Sequoia Capital, was asked by Charlie Rose why Sequoia was so successful. Moritz mentioned longevity,

Not “growth” or “brains” or “insight.” The ability to stick around for a long time, without wiping out or being forced to give up, is what makes the biggest difference

Compounding only works if you can give an asset years and years to grow. It’s like planting oak trees: A year of growth will never show much progress, 10 years can make a meaningful difference, and 50 years can create something absolutely extraordinary.

But getting and keeping that extraordinary growth requires surviving all the unpredictable ups and downs that everyone inevitably experiences over time.

We can spend years trying to figure out how Buffett achieved his investment returns: how he found the best companies, the cheapest stocks, the best managers. That’s hard. Less hard but equally important is pointing out what he didn’t do:

He didn’t get carried away with debt, didn’t panic, and sell during the 14 recessions, and didn’t rely on others’ money

He survived. Survival gave him longevity. That single point is what matters most when describing his success.

No one wants to hold cash during a bull market. They want to own assets that go up a lot. You look and feel conservative holding cash during a bull market, because you become acutely aware of how much return you’re giving up by not owning the good stuff.

Compounding doesn’t rely on earning big returns. Merely good returns sustained uninterrupted for the longest period of time – especially in times of chaos and havoc – will always win.

Planning is important, but the most important part of every plan is to plan on the plan not going according to plan.

A good plan doesn’t pretend this weren’t true; it embraces it and emphasizes room for error.

2) Risk & Reputation

we often decide whether a decision is good or not based on its outcome. It’s what poker players call “resulting”. In other words, if something works out well, we think that the strategy was great, else it’s ridiculed.

Human nature doesn’t change as fast. If one looks at the shareholding pattern of winning stocks vs losing stocks, the dominant feature is that losing stocks have their shareholding dominated by Retail while Institutions dominate the shareholding list of winning stocks.

On Twitter Bios, one thing I observe is “Not SEBI Registered” but whose entire timeline is filled with advice on what to buy / sell, etcetera. Many of them have breached the 100K mark in terms of the number of followers. On the other hand, there are real fund managers managing thousands of crores of funds and having a followership of a few thousands.

The thing about influencers is that there is a cost. If an influencer is trying to sell you a lipstick, the cost is limited because regardless of how much one loves that influencer, one won’t spend all his savings on it. A financial influencer on the other hand can devastate savings built over a long period of time.

These days reputations are built on Social Media. More the followers you have, more the belief that you know something. As much as long term investing in Index funds may yield the best return for the buck for most investors, today’s social media icons are mostly engaged in talking about how easy money can be made trading derivatives.

another favorite area for many is Nano Caps. Stocks are talked up with stories that seem to suggest that this is the next best thing only for many to crumble in the coming months / years

When something is going well, questioning is never easy. Other than in hindsight, it’s never easy to sit out either for the longer a fad runs, the longer one feels stupid. Costly errors are made because we, despite all that we know and understand, want to be part of the herd.

3) Re-rating: The X factor in multi-bagger returns

Understanding what contributes to stocks getting re-rated by the market is therefore as important to identifying multi-baggers as poring over excel sheets.

Margin transition

When analysts screen for ‘quality’ companies to invest in, a key metric they look for is a high operating profit margin (OPM). A high OPM is a sign that the company enjoys a wide ‘moat’ - the ability to charge its customers a sizeable markup over costs, irrespective of economic or business cycles. Moats are a holy grail for equity investors; therefore, companies that manage to move their OPMs into a higher orbit on a sustainable basis are often candidates for a big re-rating.

Example - Marico

Execution prowess

Ability to make the right capital allocation decisions and execute projects on the ground.

Example - Deepak Nitrite

From cyclical to secular

Predictability is a rare quality in the uncertain world of equity investing. Companies that manage to transition their cyclical business into one with secular growth are often ripe candidates for a PE re-rating.

Example - Carborundum Universal

New addressable markets

The larger the market opportunity a company faces, the higher the PE it enjoys. Therefore, when a company operating in a mature sector turns its sights to a new sunrise sector with high growth or profit potential, the market gets fired up to re-rate the stock

Example - Tata Consumer Products (TCPL)

Change in sector perception

While thus far we have seen company-specific cases of re-rating, a more common occurrence is the market bidding up the PE multiple of an entire sector because its perception of it has undergone a sea change.

Example - Auto ancillary stocks, Uno Minda

Every sector that has enjoyed a re-rating for good fundamental reasons, there are many that get re-rated on the back of fanciful themes or big-picture ideas without any improvements in the underlying fundamentals. In such cases, where earnings fail to catch up with the exalted PE multiples, big stock price reverses are bound to follow.

Example: Building material & Diagnostic chains

(Don’t Consider stock names as recommendations)

4) What Really Matters?

What Doesn’t Matter: Short-Term Events

Most investors can’t do a superior job of predicting short-term phenomena like these.

Thus, they shouldn’t put much stock in opinions on these subjects (theirs or those of others).

They’re unlikely to make major changes in their portfolios in response to these opinions.

The changes they do make are unlikely to be consistently right.

Thus, these aren’t the things that matter.

If everyone knows rates are about to rise, what difference does it make which month the process starts?” Investors probably think asking such questions is part of behaving professionally, but I doubt they could explain why.

The vast majority of investors can’t know for sure what macro events lie just ahead or how the markets will react to the things that do happen. In summary, most forecasts are extrapolations, and most of the time things don’t change, so extrapolations are usually correct, but not particularly profitable. On the other hand, accurate forecasts of deviations from trends can be very profitable, but they’re hard to make and hard to act on. These are some of the reasons why most people can’t predict the future well enough to repeatably produce superior performance.

One of the critical mistakes people are guilty of – we see it all the time in the media – is believing that changes in security prices are the result of events: that favorable events lead to rising prices and negative events lead to falling prices. Security prices are determined by events and how investors react to those events, which is largely a function of how the events stack up against investors’ expectations.

Investors can become experts regarding a few companies and their securities, but no one is likely to know enough about macro events to (a) be able to understand the macro expectations that underlie the prices of securities, (b) anticipate the broad events, and (c) predict how those securities will react.

Further, in the short term, security prices are highly susceptible to random and exogenous events that can swamp the impact of fundamental events. Macro events and the ups and downs of companies’ near-term fortunes are unpredictable and not necessarily indicative of – or relevant to – companies’ long-term prospects. So little attention should be paid to them.

No one should be fooled into thinking security pricing is a dependable process that accurately follows a set of rules. Due to the presence of so much uncertainty, most investors are unable to improve their results by focusing on the short term.

What accounts for this? It must be the fact that, in the short term, the ups and downs of prices are influenced far more by swings in investor psychology than by changes in companies’ long-term prospects.

What Doesn’t Matter: The Trading Mentality

If you ask Warren Buffett to describe the foundation of his approach to investing, he’ll probably start by insisting that stocks should be thought of as ownership interests in companies. Most people don’t start companies with the goal of selling them in the short term, but rather they seek to operate them, enjoy profitability, and expand the business.

But I think that’s rarely the case. Most people buy stocks with the goal of selling them at a higher price, thinking they’re for trading, not for owning.

The DALBAR Institute 2012 study showed that investors receive three percentage points less per year than the S&P 500 generated from 1992 to 2012, and the average holding period for a typical investor is six months. Six Months!! When you hold a stock for less than a year, you are not using the stock market to acquire business ownership positions and participate in the growth of that business. Instead, you are just guessing at short-term news and expectations, and your returns are based on how other people react to that news information.

Every buyer is motivated by the belief that the stock will eventually be worth more than today’s price. The key question is what type of thinking underlies these purchases. Are the buyers buying because this is a company they’d like to own a piece of for years? Or are they merely betting that the price will go up?

Each time a stock is traded, one side is wrong and one is right.

en Graham famously said, “In the short run, a market is a voting machine, but in the long run, it is a weighing machine.” While none of this is easy, as Charlie Munger once told me, carefully weighing long-term merit should produce better results than trying to guess at short-term swings in popularity.

What Doesn’t Matter: Short-Term Performance

There are three ingredients for success during good times – aggressiveness, timing, and skill – and if you have enough aggressiveness at the right time, you don’t need that much skill. We all know that in good times, the highest returns often go to the person whose portfolio incorporates the most risk, beta, and correlation. Having such a portfolio isn’t a mark of distinction or insight if the investor is a perma-bull who’s always positioned aggressively. Finally, random events can have an overwhelming impact on returns – in either direction – in a given quarter or year.

The quality of a decision cannot be determined from the outcome alone.

Obviously, no one should attach much significance to returns in one quarter or year. Investment performance is simply one result drawn from the full range of returns that could have materialized, and in the short term, it can be heavily influenced by random events. Thus, a single quarter’s return is likely to be a very weak indicator of an investor’s ability, if that.

We know short-term performance doesn’t matter much. And yet, most of the investment committees I’ve sat on have had the latest quarter’s performance as the first item on the agenda and devoted a meaningful portion of each meeting to it.

What Doesn’t Matter: Volatility

I strongly disagree with people who consider it the definition or essence of risk. I define risk as the probability of a bad outcome, and volatility is, at best, an indicator of the presence of risk. But volatility is not risk. That’s all I’m going to say on that subject.

The Sharpe ratio may hint at risk-adjusted performance in the same way that volatility hints at risk, but since volatility isn’t risk, the Sharpe ratio is a very imperfect measure.

Strategists and the media often warn that “there may be volatility ahead.” What they really mean is “there may be price declines ahead.” No one worries about, or minds experiencing, volatility to the upside.)

Volatility is just a temporary phenomenon (assuming you survive it financially), and most investors shouldn’t attach as much importance to it as they seem to.

Investors should take advantage of their ability to withstand volatility since many investments with the potential for high returns might be susceptible to substantial fluctuations.

Warren Buffett always puts it best, and on this topic he usefully said, “We prefer a lumpy 15% return to a smooth 12% return.” Investors who’d rather have the reverse – who find a smooth 12% preferable to a lumpy 15% – should ask themselves whether their aversion to volatility is mostly financial or mostly emotional.

In many cases, people accord volatility far more importance than they should.

What Doesn’t Matter: Hyper-Activity

When I was a boy, there was a popular saying: Don’t just sit there; do something. But for investing, I’d invert it: Don’t just do something; sit there.

Develop the mindset that you don’t make money on what you buy and sell; you make money (hopefully) on what you hold. Think more. Trade less. Make fewer, but more consequential, trades. Over-diversification reduces the importance of each trade; thus it can allow investors to take actions without adequate investigation or great conviction.

I’m not saying it’s worth dying to improve investment performance, but it might be a good idea for investors to simulate that condition by sitting on their hands.

So What Does Matter?

What really matters is the performance of your holdings over the next five or ten years (or more) and how the value at the end of the period compares to the amount you invested and to your needs. Some people say the long run is a series of short runs, and if you get those right, you’ll enjoy success in the long run. They might think the route to success consists of trading often in order to capitalize on relative value assessments, predictions regarding swings in popularity, and forecasts of macro events. I obviously do not.

I think most people would be more successful if they focused less on the short-run or macro trends and instead worked hard to gain superior insight concerning the outlook for fundamentals over multi-year periods in the future. They should:

study companies and securities, assessing things such as their earnings potential;

buy the ones that can be purchased at attractive prices relative to their potential;

hold onto them as long as the company’s earnings outlook and the attractiveness of the price remain intact; and

make changes only when those things can’t be reconfirmed, or when something better comes along.

I’m going to outline some of what I think are key elements to remember.

Forget the short run

Decide whether your approach will lean more toward aggressiveness or defensiveness.

Think about what your normal risk posture should be

Adopt a healthy attitude toward return and risk.

Insist on an adequate margin of safety, or the ability to weather periods when things go less well than you expected.

Stop trying to predict the macro;

Recognize that psychology swings much more than fundamentals, and usually in the wrong direction or at the wrong time.

Study conditions in the investment environment – especially investor behavior – and consider where things stand in terms of the cycle.

Think about the 10.5% yearly return of the S&P 500 Index (or its predecessors) since 1926 and the fact that this would have turned $1 into over $13,000 by now, even though the period witnessed 16 recessions, one Great Depression, several wars, one World War, a global pandemic, and many instances of geopolitical turmoil.

Think of participating in the long-term performance of the average as the main event and the active efforts to improve on it as “embroidery around the edges.”

Investors should find a way to keep their hands off their portfolios most of the time.

A Special Word in Closing: Asymmetry

“Asymmetry” is a concept I’ve been conscious of for decades and consider more important with every passing year. It’s my word for the essence of investment excellence and a standard against which investors should be measured.

I’m going to talk below about whether an investor has “alpha.” Alpha is technically defined as a return in excess of the benchmark return, but I prefer to think of it as a superior investing skill. It’s the ability to find and exploit inefficiencies when they’re present.

Having alpha allows an investor to enjoy profit potential that is disproportionate to lose potential: asymmetry. In my view, asymmetry is present when an investor can repeatedly do some or all of the following:

make more money in good markets than he gives back in bad markets,

have more winners than losers,

make more money on his winners than he loses on his losers,

do well when his aggressive or defensive bias proves timely but not badly when it doesn’t,

do well when his sector or strategy is in favor but not badly when it isn’t, and

construct portfolios so that most of the surprises are on the upside.

To determine whether they have alpha and produce asymmetry, we have to consider whether the aggressive investor is able to avoid the full loss that his aggressiveness alone would produce in a bad market and whether the defensive investor can avoid missing out on too much of the gain when the market does well

if an investor doesn’t have alpha, her returns won’t be asymmetrical. It’s as simple as that.

In sum, asymmetry shows up in a manager’s ability to do very well when things go his way and not too bad when they don’t.

The average of all investors’ thinking produces market prices and, obviously, average performance. Asymmetry can only be demonstrated by the relatively few people with superior skill and insight. The key lies in finding them.

Small Video Clips

➢ Mohnish Pabrai & Guy Spier Interview

Don't try hard to expand the circle of competence (28:17 to 29:32)

Mohnish talks about concentration, RJ, and Titan (45:28 to 54:27)

How to eliminate bad decisions using a mental model (59:02 to 1:00:12)

➢ Rajeev Thakkar (PPFAS) Interview - 2017

Investing in the USA (Advantages & disadvantages (21:36 to 26:11)

How hedging is done for investing in the USA And How it's beneficial for PPFAS (27:23 to 33:04)

How to find Quality business at reasonable prices (38:21 to 44:17)

Selling Criteria (44:28 to 46:26)

Investing Mistakes (46:50 to 52:15)

How to value a business? (52:35 to 56:15)

Should we act based on the market under/over-valuation (57:47 to 01:00:52)

➢ Sumeet Nagar Interview by Equitymaster

How Sumit Nagar Navidated major stock market declines/Bear market (34:55 to 39:57)

Investment time Horizon (40:10 to 41:20)

Covid Crash Experience (41:53 to 47:55)

How is it hard to value Business? (51:45 to 53:28)

Malabar Investment's Buying Criteria/Investment Process (54:06 to 57:40)

How to value business beyond P/E, P/B ratio (58:13 to 59:38)

How to assess Management Quality (59:58 to 01:10:22)

Avanti Feeds Stock Case Study (Buying to Selling) (01:11:53 to 01:16:11)

Investing mistakes/failures (01:16:40 to 01:25:00)

Selling Criteria (01:29:14 to 01:31:29)

→ Recommended books to read

A Zebra In Lion Country (If you love small-cap investing, you should read)

That’s it from my end for this week. Thanks for reading.

See you again next week!

Dhaval.

If you enjoyed this, please share it with your friend.

Loved it! 🙏🙌

Thanks for the effort, very useful.